While omnichannel marketing is emerging as a critical approach for advertisers, it relies heavily on performance in the relevant channels at the individual level, which doesn’t translate readily to aggregate analysis. At Skai, we reconcile this by looking at the different channels and publishers through a similar lens and teasing out similarities and differences, particularly for key segments of the whole.

In the Q2 2023 Quarterly Trends Report, we take this approach to commerce advertisers across channels, but what about regional differences?

For the following analysis, we focus on Europe, the Middle East, and Africa (EMEA) to see how performance compares across channels and also with respect to North America (AMER). In retail media, we will consider ad campaigns that run on specific marketplaces across Europe, the Middle East, and Africa (EMEA). For paid search, we will consider accounts that originate in and are managed out of those regions, regardless of where the ads are served.

Note: This analysis is based on accounts with fifteen consecutive months of spending at the channel level. Some outliers have been removed. Spending and cost-per-click metrics are calculated in US Dollars and converted to Euros based on the exchange rate on the last day of the quarter (30 June).

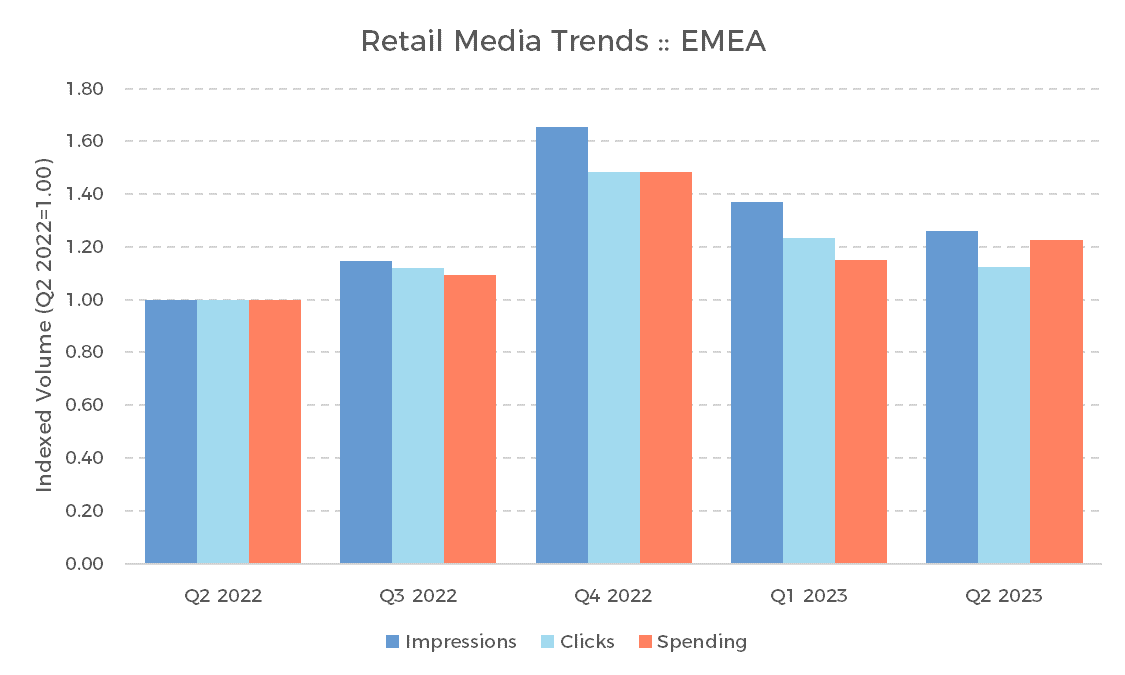

Retail Media

Overall, retail media impressions in EMEA grew 26% year-over-year (YoY) in Q2 2023. Clicks were up 13%, and spending increased 22%. By comparison, YoY spending growth in the AMER region (North America) was 34%.

One key reason for this regional difference is that the clickthrough rate (CTR) in the EMEA region decreased over the past five quarters while the AMER region increased. CTR for EMEA is down 11% YoY, although it has remained flat for the last three quarters.

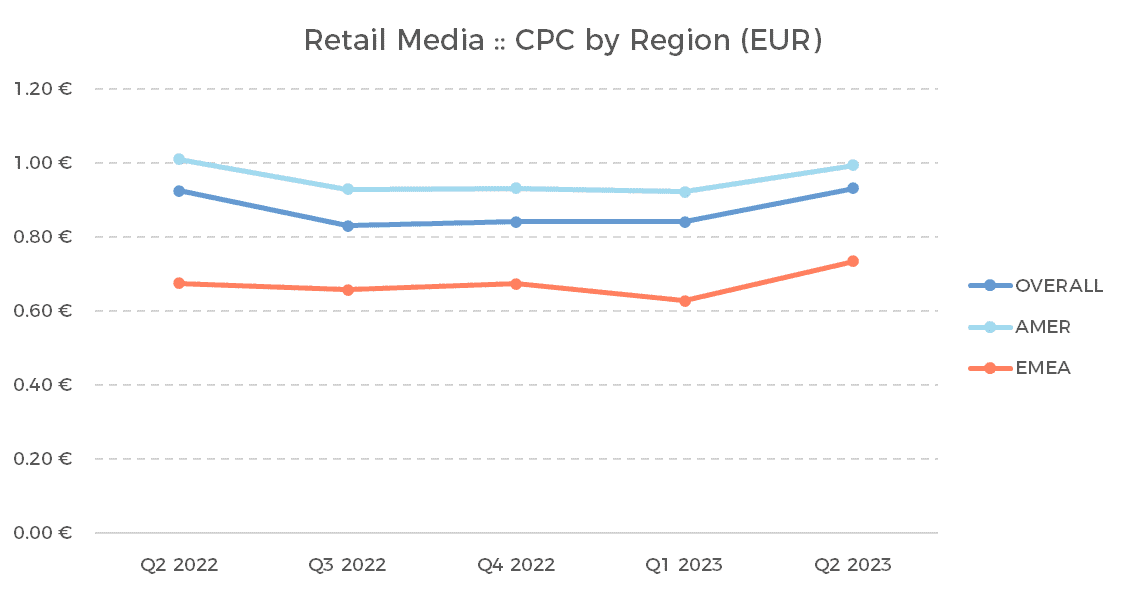

Ad prices, on the other hand, have increased 9% YoY in EMEA while they have decreased 2% in AMER. Average cost-per-click (CPC) is approximately 50% higher in the Americas, which means that this increase, when combined with the drop in clickthrough rate, was not enough to keep spending at pace.

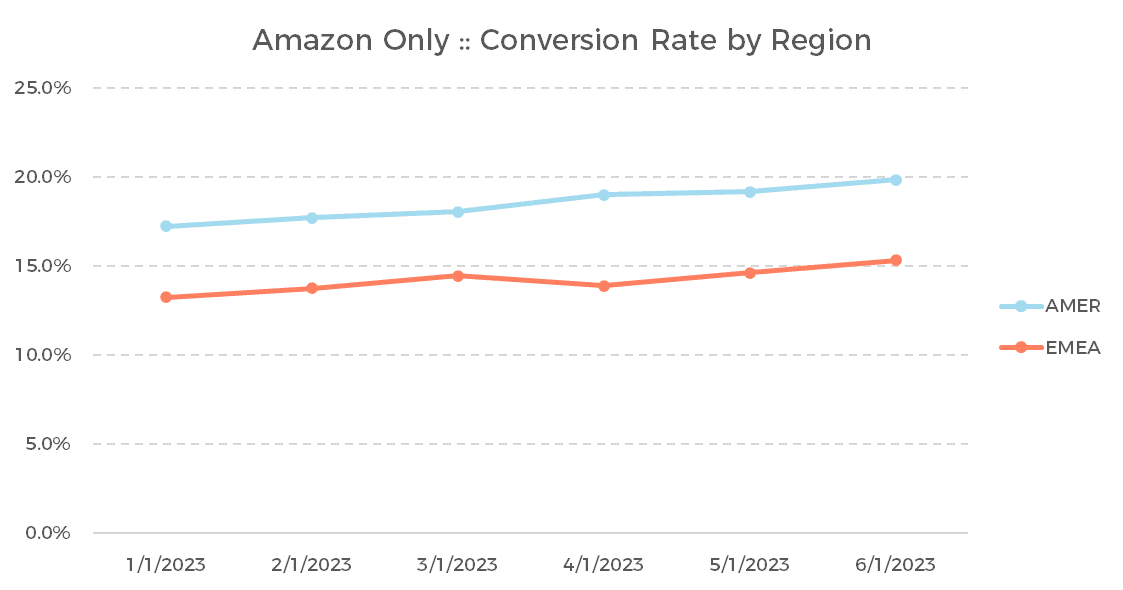

Another key trend we observed in Q2 was an increase in retail media conversion rate, which is one of the clearest indicators that consumer demand is recovering from the higher inflation rates in the second half of last year. In fact, if we look at Amazon conversion rates by month for the first six months of 2023, we see them trending upwards in both AMER and EMEA, which aligns with the quarter-over-quarter (QoQ) increases in CPC in both regions.

When conversion rates are higher, that means it takes fewer clicks to convert, and if advertisers are targeting return on ad spend (ROAS) as their primary KPI, then they can afford to pay higher CPC and still achieve their goals. Suffice it to say, this trend bodes well for the overall economic picture into the second half of the year and the holiday season.

Paid Search

For accounts managed in EMEA, paid search impressions were down 6% YoY, while clicks decreased by 2% and overall spending fell 7%. Over the same period, spending in AMER grew 7%.

One key driver of this behavior is ad price. While Average CPC dropped 4% in both regions, how they got there is much different. EMEA ad prices have been slowly dropping since Q4, while in AMER, there was a significant increase in CPC from Q1 to Q2. Had that happened in EMEA, the YoY spending numbers would have come out much differently.

The gap between EMEA and AMER prices could be due to a different mix of ad types and formats. Branded keywords and mobile ads, for example, typically have lower CPC.

Clickthrough rate in EMEA was down 4% QoQ and up 4% YoY, compared to AMER, which was up 9% over last year. In general, CTR has been consistently higher in EMEA than AMER, which once again may come down to the relative share of certain segments with higher rates. Branded keywords, in particular, typically demonstrate both lower CPC (due to higher Quality Score) and higher CTR.

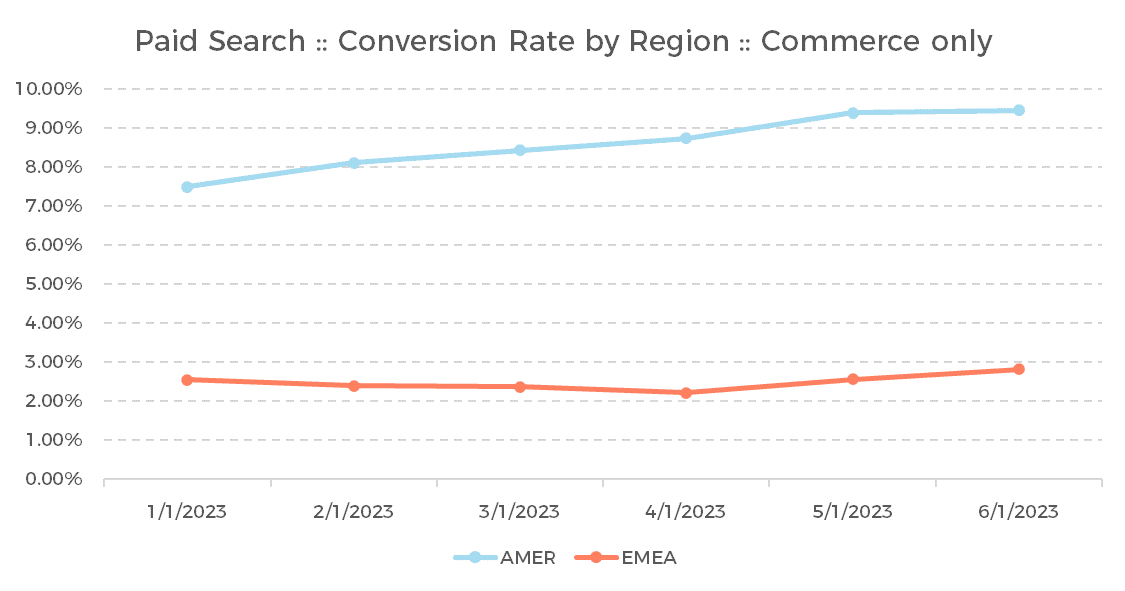

Once more, it is useful to look at how conversion rates may affect these trends. Looking at paid search conversion rates for commerce advertisers, we see that while AMER drives the overall trend, EMEA is seeing those rates pick up starting in April. With search ads being just a bit farther from the final point of conversion and with the economies across Europe lagging somewhat behind the United States, it stands to reason that the increase is somewhat delayed in the region. This, too, should bode well for H2 performance.

Unlike CPC or CTR, the disparity in absolute conversion rates between the regions is more complex than just the mix of ads. Different industry categories have different purchase funnels, both in terms of time and threshold, so we should not read much into this difference.

While EMEA can be described as underperforming relative to AMER across several metrics, some of the fundamental trends driving growth exist in both regions, just with different magnitudes and different timing. If those trends continue, we are likely to see increased performance in the second half of 2023, which unlocks additional ad budgets as we move towards the all-important fourth quarter.

Skai is the only omnichannel marketing platform for performance advertising

We’re helping marketers connect the walled gardens across retail media, paid search, paid social, and app marketing, making true omnichannel performance marketing a reality. We’ll keep you at the forefront of the digital evolution with data and insights, marketing execution, and measurement tools that work together to drive powerful brand growth. Client results include:

- 461% increase in Amazon Ads ROAS and 57% increase in page traffic for Bondi Sands

- 280% increase in installs for DraftKings

- 10% increase in new account openings for Royal Bank of Canada

- 756% increase in conversions for New York Magazine

- 600% increase in Facebook leads for Inova

For more information or to see our cutting-edge innovation firsthand, please schedule a quick demo today!