KPIs Across Paid Search, Social Advertising, and Ecommerce Channel Advertising

For most marketers, September is generally focused on getting ready for the big Q4 holiday season. It’s not a time to do a lot of testing new channels or messaging, but rather to steward campaigns that have already been optimized throughout the year.

Of course, this September was a bit different than any other September in recent memory due to the chaotic year that 2020 has been so far. Advertisers spent a little more in September than they did in August which could be both a sign of continued recovery as well as warming up for the start of the holiday shopping season.

Advertisers also paid a bit more in terms of ad costs across paid search CPCs, social advertising CPMs, and ecommerce channel advertising CPCs. All in all, 4 in 10 Skai accounts in both Paid Search and Ecommerce Advertising saw CPCs go up at least 10%, and nearly 7 in 10 Paid Social accounts had CPMs increase by that amount. With the high-demand of the holidays coming fast, this may influence the way you think about how aggressive you should be with your bids this quarter.

This is our second month of this new benchmarking series. As always, with any benchmark information, your mileage may vary, but we hope this provides a bit more context for you as a marketer as you navigate the ups and downs of your program’s performance.

Monthly Paid Media Spend Snapshot – September 2020

Methodology note. For the purpose of these monthly benchmarks, only Skai accounts with spend above a minimum threshold for the previous three months are included in this analysis.

Paid Search spending

The largest share of search accounts saw spending stay within 5% of last month, while spending increases just edged out decreases overall. In other words, September did not show much discernable budget movement one way or the other.

- 35% of paid search accounts spent +10% or more in September versus August, compared to 32% who spent -10% or less (+3% differential)

- 8% of accounts spent +50% or more in September versus August, compared to 5% of accounts spending -50% or less (+3% differential)

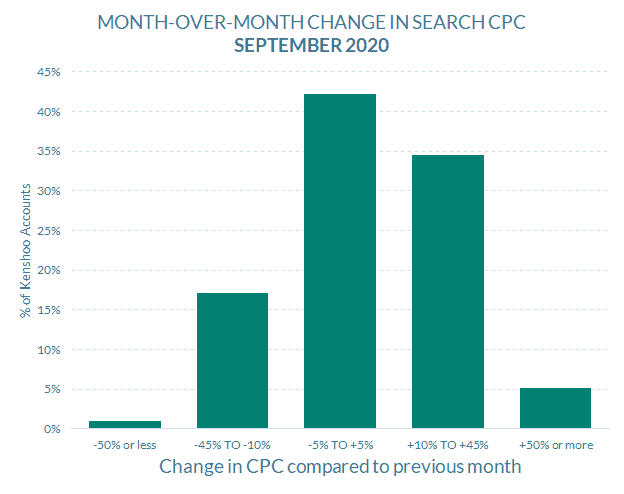

Paid Search CPCs

As a whole, click prices were more likely to go up than down for search marketers in September, although they were likelier still to mostly stay put.

- 40% of paid search accounts paid +10% or more per click in September versus August, compared to 18% who paid -10% or less (+22% differential)

- 5% of accounts paid +50% or more in September versus August, compared to 1% of accounts paying -50% or less (+4% differential)

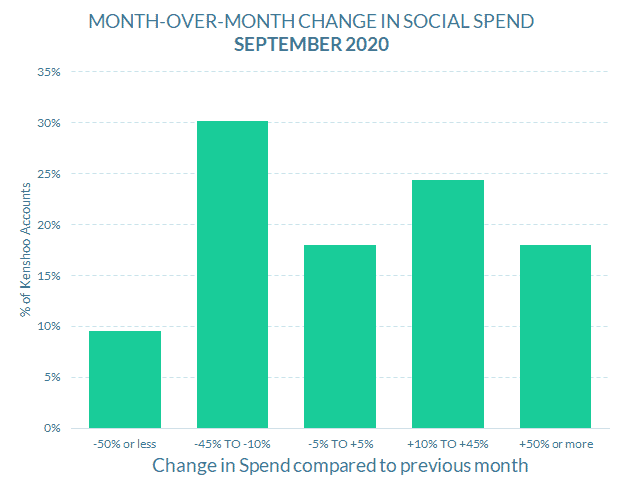

Social advertising spending

Spending increased more at the margins–accounts spending much more compared to much less than last month–but broadly speaking, spending seemed as likely to increase as decrease last month.

- 42% of paid social accounts spent +10% or more in September versus August, compared to 40% who spent -10% or less (+2% differential)

- 18% of accounts spent +50% or more in September versus August, compared to 10% of accounts spending -50% or less (+8% differential)

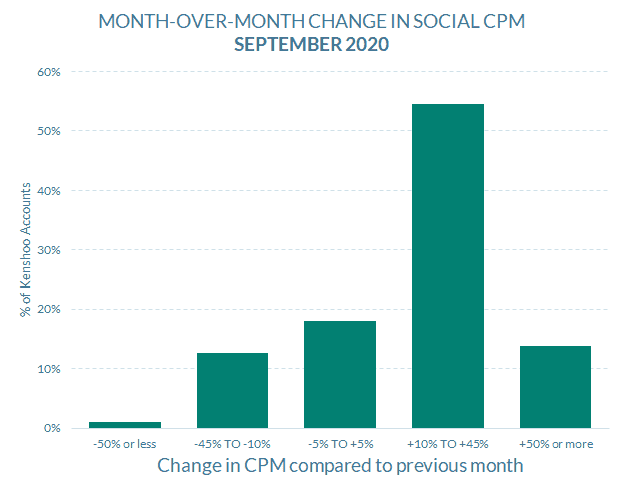

Social advertising CPMs

Social advertising CPMs

Social advertising CPMs

Social advertising CPMsAn outright majority of paid social accounts saw impression prices increase between 10% and 45% compared to last month. Combined with the spending trends, this implies that advertisers are honing in on more lucrative, more expensive and smaller audiences.

- 68% of paid social accounts paid +10% or more per thousand impressions in September versus August, compared to 14% who paid -10% or less (+54% differential)

- 14% of accounts paid +50% or more per thousand impressions in September versus August, compared to 1% of accounts paying -50% or less (+13% differential)

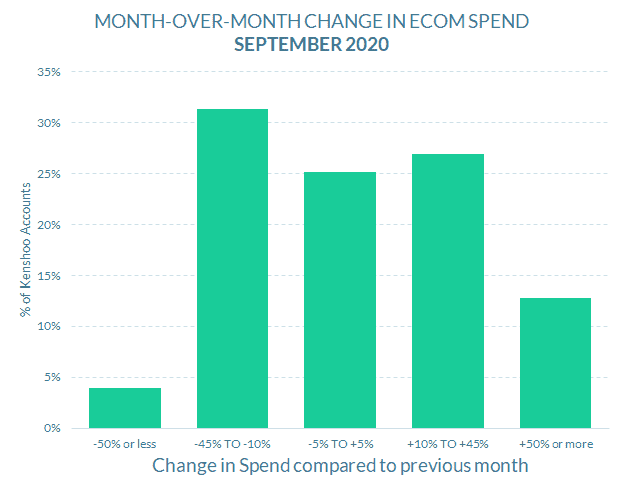

Ecommerce channel advertising spending

Ecommerce channel advertising spending

Ecommerce channel advertising spendingJust over a third of Ecommerce accounts spent less in September than August, although overall, more advertisers increased budgets by at least ten percent.

- 40% of ecommerce advertising accounts spent +10% or more in September versus August, compared to 35% who spent -10% or less (+5% differential)

- 13% of accounts spent +50% or more in September versus August, compared to 4% of accounts spending -50% or less (+9% differential)

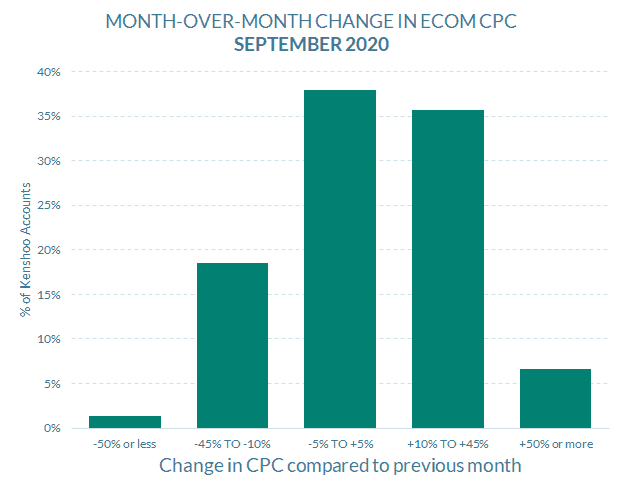

Ecommerce channel advertising CPCs

Higher prices for a larger share of advertisers is one reason spending is also up for more of those advertisers.

- 42% of ecommerce advertising accounts paid +10% or more per click in September versus August, compared to 20% who paid -10% or less (+22% differential)

- 7% of accounts paid +50% or more per click in September compared to August, versus 1% of accounts paying -50% or less (+6% differential)

Check out more resources from Skai

Check out more resources from Skai

Check out more resources from SkaiCome back in September for our next monthly trends post. Until then, you can dive into more of our research via our Quarterly Trends Reports hub and our COVID-19 Marketing Resource Center.

And please visit the Skai blog and Research & Reports page for ongoing insights, analysis, and interviews on all things related to digital advertising.