Spending and Pricing Trends Across Paid Search, Social Advertising, and Ecommerce Channel Advertising

Goodbye 2020!

Flipping the calendar doesn’t really separate us from what was going on just a week ago, but it certainly feels like a fresh start, and a welcome one at that. Still, we want to see just what happened in December before we go about the business of the new year.

Early analysis points to a very healthy 2020 Q4 as advertisers put a lot of faith (and ad dollars) into the end-of-the-year holiday season to help offset a historically down year, while increased internet use for our increasingly home-based lifestyles amplified that faith. And those ad dollars.

December can always go one of two ways for advertisers. Brands can look at their bigger budgets and big results from November, particularly across the Thanksgiving weekend, and ease up as the number of days until Christmas shrinks. Or they can double down in the home stretch, committing to increased spending into the last month of the year in order to take advantage of consumers still hunting for deals.

Our monthly benchmarking series is intended to shed light on just how many marketers fall into each of those camps. How many brands increased spending in December? How many shrank their budgets?

We also look at how ad prices square with those channel trends. For example, in Paid Search and Ecommerce Channel Advertising (ECA), click costs were down as demand started to loosen up. But in Social Advertising—where advertisers generally have broader objectives than just selling products—ad costs stayed higher.

Now, with 2020 and the big holiday season behind us, it’s back to the grind for marketers. Generally, January levels fall back to “normal” from Q4 as advertisers reset and begin implementing their revised plans for the new calendar year. Check back in next month’s post to review January 2021 numbers to see how it’s trending.

This is a continuation of our monthly paid media snapshot series. As with any benchmark, your mileage may vary, but we hope this provides a bit more context for you as a marketer as you navigate the ups and downs of your program’s performance.

Monthly Paid Media Spend Snapshot – Dec 2020

Methodology note. For the purpose of these monthly benchmarks, only Skai accounts with spend above a minimum threshold for the previous three months are included in this analysis.

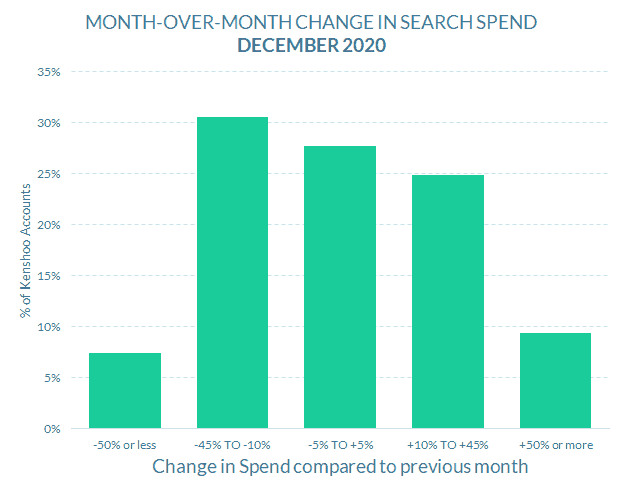

Paid Search spending

With both Black Friday and Cyber Monday in the rearview mirror, more advertisers saw spending decrease than increase in December.

- 34% of paid search accounts spent +10% or more in December versus November, compared to 38% who spent -10% or less (-4% differential)

- 9% of accounts spent +50% or more in December versus November, compared to 7% of accounts spending -50% or less (+2% differential)

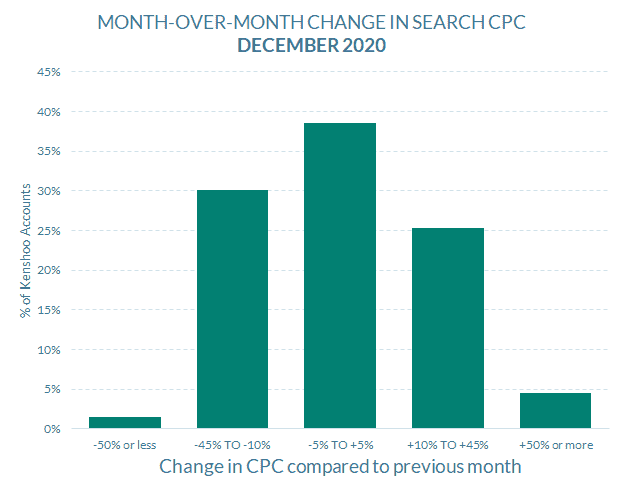

Paid Search CPCs

Search ad pricing also decreased for more advertisers as the holiday premiums receded at least slightly after the Cyber 5 weekend.

- 30% of paid search accounts paid +10% or more per click in December versus November, compared to 32% who paid -10% or less (-2% differential)

- 4% of accounts paid +50% or more per click in December versus November, compared to 1% of accounts paying -50% or less (+3% differential)

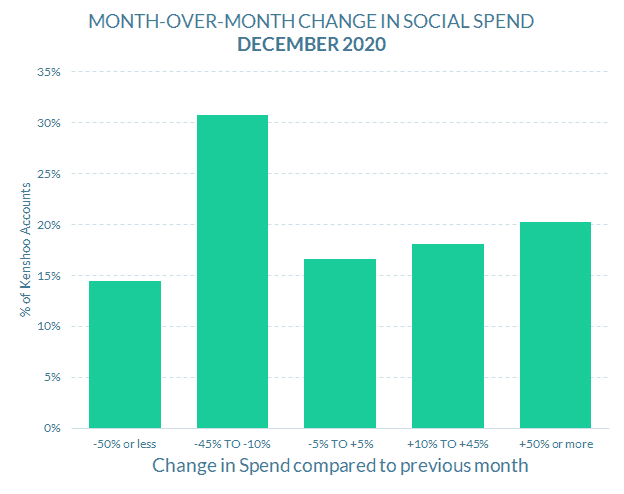

Social advertising spending

With the big holiday shopping weekend and the US election in November, the bulk of advertisers saw spending decline in December, although 1 in 5 increased budgets by at least 50%.

- 38% of paid social accounts spent +10% or more in December versus November, compared to 45% who spent -10% or less (-7% differential)

- 20% of accounts spent +50% or more in December versus November, compared to 14% of accounts spending -50% or less (+6% differential)

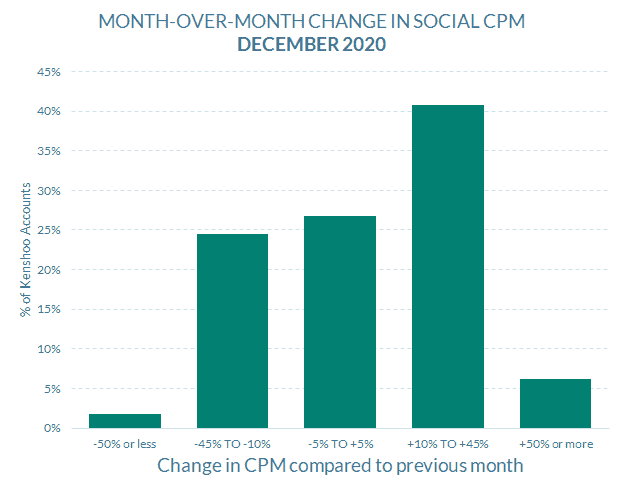

Social advertising CPMs

Increasing prices for just over 40% of advertisers could be one factor driving the segment who saw larger budget increases in December.

- 47% of paid social accounts paid +10% or more per thousand impressions in December versus November, compared to 26% who paid -10% or less (+21% differential)

- 6% of accounts paid +50% or more per thousand impressions in December versus November, compared to 2% of accounts paying -50% or less (+4% differential)

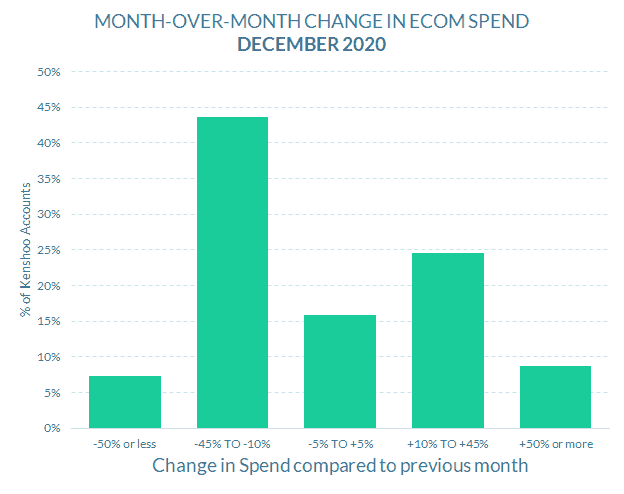

Ecommerce channel advertising spending

1 out of 3 advertisers in the Ecommerce channel kept the pedal to the metal in December, while half saw a decrease in ad budgets after the frenzy of November and the long Thanksgiving weekend.

- 33% of ecommerce advertising accounts spent +10% or more in December versus November, compared to 51% who spent -10% or less (-18% differential)

- 9% of accounts spent +50% or more in December versus November, compared to 7% of accounts spending -50% or less (+2% differential)

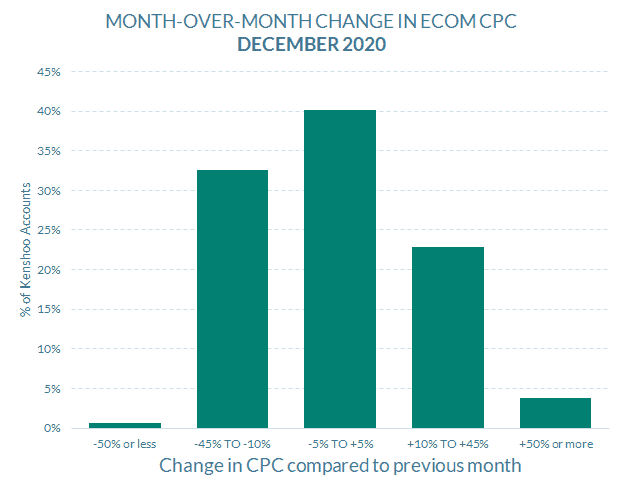

Ecommerce channel advertising CPCs

Advertisers in the Ecommerce channel were more likely to see click prices go down in December than up, reflecting the more intense competition in November.

- 27% of ecommerce advertising accounts paid +10% or more per click in December versus November, compared to 33% who paid -10% or less (-6% differential)

- 4% of accounts paid +50% or more per click in December compared to November, versus 1% of accounts paying -50% or less (+3% differential)

Check out more resources from Skai

Come back in February for our next monthly trends post. Until then, you can dive into more of our research via our Quarterly Trends Reports hub and our COVID-19 Marketing Resource Center.

And please visit the Skai blog and Research & Reports page for ongoing insights, analysis, and interviews on all things related to digital advertising.