Spending and Pricing Trends Across Paid Search, Social Advertising, and Retail Media

February is the shortest month of the year. The end-of-year holiday shopping season is retreating into the rearview mirror, and budgets are settling down accordingly.

As reported in our Q4 2020 Skai Quarterly Trends Report, brands went big during that holiday season, and while spending typically eases up in the first months of a new year, we know that last year was anything but typical.

While February of 2020 may have only seen the very beginnings of the impact of a global pandemic on advertisers and advertising campaigns, that impact was still being felt through the end of the year, so February of this year could go a number of different ways as a result.

Ultimately, in a month that had 10% fewer days than the previous month, spending reflected that disparity. A slightly larger share of brands pulled back a bit on spending in February compared to January’s start of the year, while at least a third of brands upped their investment somewhat. All in all, channel spending across Paid Search, Social Advertising, and Retail Media was fairly stable.

This is a continuation of our monthly paid media snapshot series. As with any benchmark, your mileage may vary, but we hope this provides a bit more context for you as a marketer as you navigate the ups and downs of your program’s performance.

Monthly Paid Media Spend Snapshot – February 2021

Methodology note. For the purpose of these monthly benchmarks, only Skai accounts with spend above a minimum threshold for the previous three months are included in this analysis.

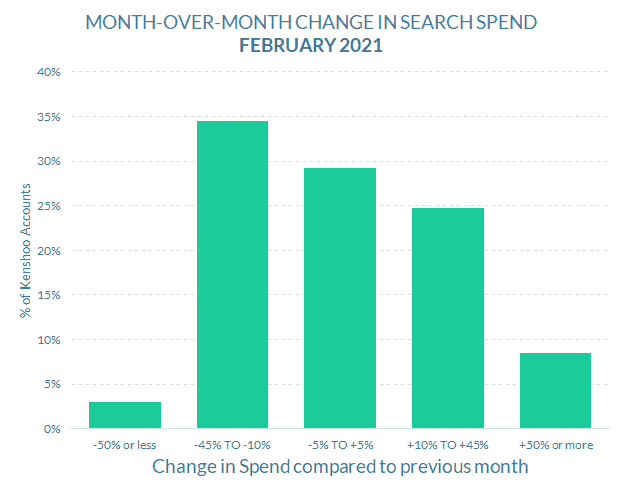

Paid Search spending

Advertisers across paid search showed a slightly higher tendency to reduce spending in February compared to January.

- 33% of paid search accounts spent +10% or more in February versus January, compared to 38% who spent -10% or less (-5% differential)

- 9% of accounts spent +50% or more in February versus January, compared to 3% of accounts spending -50% or less (+6% differential)

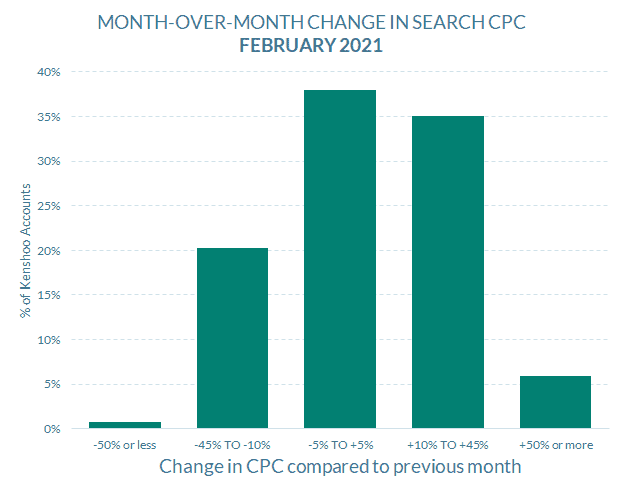

Paid Search CPCs

Search ad prices in February were more likely to have gone up than down compared to the previous month, which implies that the spending trend was driven by lower volumes and not pricing.

- 41% of paid search accounts paid +10% or more per click in February versus January, compared to 21% who paid -10% or less (+20% differential)

- 6% of accounts paid +50% or more per click in February versus January, compared to 1% of accounts paying -50% or less (+5% differential)

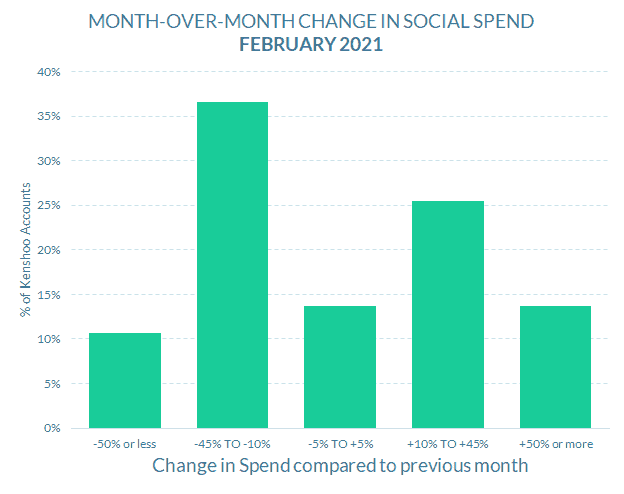

Social Advertising spending

Social advertising saw the greatest share of accounts with a monthly increase in spending across channels, but the small share of budgets remaining unchanged led to an overall picture of less spending in February.

- 39% of paid social accounts spent +10% or more in February versus January, compared to 47% who spent -10% or less (-8% differential)

- 14% of accounts spent +50% or more in February versus January, compared to 11% of accounts spending -50% or less (+3% differential)

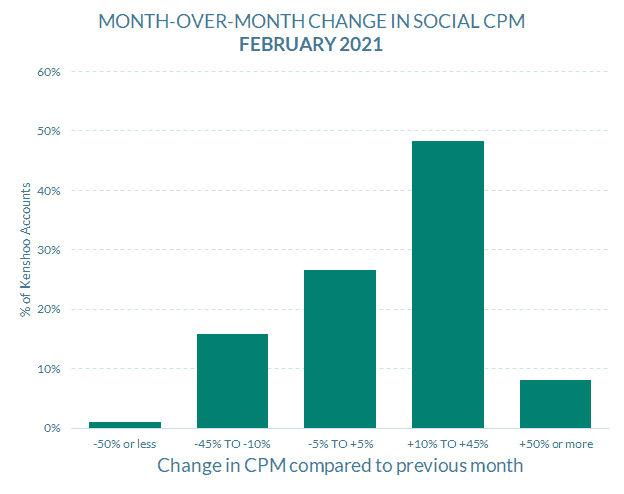

Social Advertising CPMs

The majority of social advertisers paid higher prices per thousand impressions in February compared to January, which could result from competition or from narrower targeting.

- 56% of paid social accounts paid +10% or more per thousand impressions in February versus January, compared to 17% who paid -10% or less (+39% differential)

- 8% of accounts paid +50% or more per thousand impressions in February versus January, compared to 1% of accounts paying -50% or less (+7% differential)

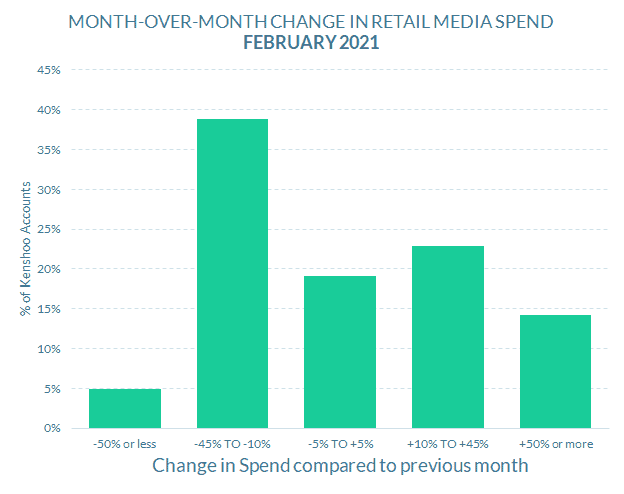

Retail Media spending

One reason why budgets were more likely to be lower in February across Retail Media advertisers may be that there were only four Sundays in February compared to January, and Sunday typically one of the highest-spending days of the week for the channel.

- 37% of retail media advertising accounts spent +10% or more in February versus January, compared to 44% who spent -10% or less (-7% differential)

- 14% of accounts spent +50% or more in February versus January, compared to 5% of accounts spending -50% or less (+9% differential)

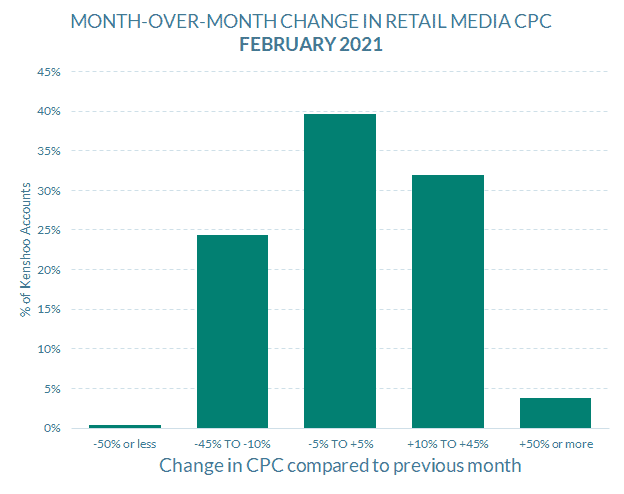

Retail Media CPCs

Ad prices in Retail Media were largely steady in February, with perhaps just a slight tendency to have gone up.

- 36% of retail media advertising accounts paid +10% or more per click in February versus January, compared to 25% who paid -10% or less (+11% differential)

- 4% of accounts paid +50% or more per click in February compared to January, versus % of accounts paying -50% or less (+4% differential)

Check out more resources from Skai

Come back in February for our next monthly trends post. Until then, you can dive into more of our research via our Quarterly Trends Reports hub and our COVID-19 Marketing Resource Center.

And please visit the Skai blog and Research & Reports page for ongoing insights, analysis, and interviews on all things related to digital advertising.