Summary

Cyber Five 2024 smashed records with $41.1 billion in online sales, marking the biggest shopping spree in history! Black Friday led the way with a staggering 92% surge in retail media spending, while Cyber Monday dazzled as the largest online shopping day ever, raking in $13.3 billion. Dive into the insights behind these trends to sharpen your strategies and drive even greater success.

Last updated: December 22, 2025

Cyber Monday 2024 set a new benchmark as the largest online shopping day in U.S. history, with consumers spending a record $13.3 billion—a 7.3% year-over-year increase that slightly exceeded expectations. During peak hours from 8 to 10 p.m. EST, shoppers spent $15.8 million per minute, contributing to an impressive Cyber Five period. In total, online sales across these five critical days reached $41.1 billion, up 8.2% from last year, with Black Friday and Thanksgiving both delivering strong performances at $10.8 billion (+10.2% YOY and a record-breaker for that day) and $6.1 billion (+8.8% YOY), respectively.

As part of our annual Cyber Five 2024 recap, we build on insights from our Black Friday 2024 analysis, which revealed the growing dominance of retail media, paid search, and paid social in driving conversions. Black Friday’s 92% surge in retail media spending set the tone for the week and underscored the importance of diversifying channels for a comprehensive holiday strategy. These trends continued through the Cyber Five period, offering critical data for marketers looking to refine their peak event strategies.

What can marketers learn from these results? This year’s Cyber Five wasn’t just about record-breaking numbers—it highlighted evolving trends in consumer behavior and advertising performance. Retail media continues to surge, becoming the go-to channel for peak shopping days like Black Friday, but Cyber Monday also showed how strategic ad spend can drive results amidst shifting consumer preferences. Across paid search and paid social, platform-specific strategies were essential, with diverse performance metrics demonstrating the need for precision and flexibility in campaign execution. Marketers now have deeper insights into the dynamics of consumer intent and engagement, which will be invaluable for optimizing future campaigns throughout the season.

And let’s not forget the full value of this elevated Cyber Five spending may play out in the coming weeks and months. While these campaigns are designed to drive immediate sales, many consumers were exposed to brands for the first time or had their top-of-mind awareness reinforced. These early touchpoints will likely lead to future conversions as consumers continue their shopping journey and return to brands they’ve interacted with during the Cyber Five.

As we dive into the analysis, we’ll explore each channel’s key trends and takeaways, offering marketers a detailed understanding of what happened and how to apply these insights to future holiday campaigns.

Cyber 5 2024 Key Takeaways:

- Retail Media: Retail media continues to surge in importance, with Black Friday showing its massive impact on conversions and spend. It’s becoming the go-to channel during peak shopping days and is crucial for driving results across the entire holiday season.

- Paid Search: Cyber Monday surpassed Black Friday in spend, driven by sharp CPC increases. Early activity across other channels during the Cyber Five primes consumers to search, making paid search a channel that must be managed daily to capture growing demand.

- Paid Social: TikTok’s 52% impression growth vs. Meta’s CPM-driven performance raises the question: are we seeing a changing of the guard? TikTok is making its mark, and marketers should rethink their strategies to stay ahead of the curve.

Micro-answer: The five biggest online shopping days.

What makes a full season retail media strategy essential?

- Retail media intensity spikes on Black Friday then sustains.

- Black Friday leads conversion lift, but post Cyber Monday demand persists.

- Retail media performance during Cyber Five rewards brands that plan beyond single day peaks. Prioritizing Black Friday for scale while maintaining flexibility through Cyber Monday and the following days helps capture latent demand, protect share of voice, and convert shoppers who continue deal hunting across the full season.

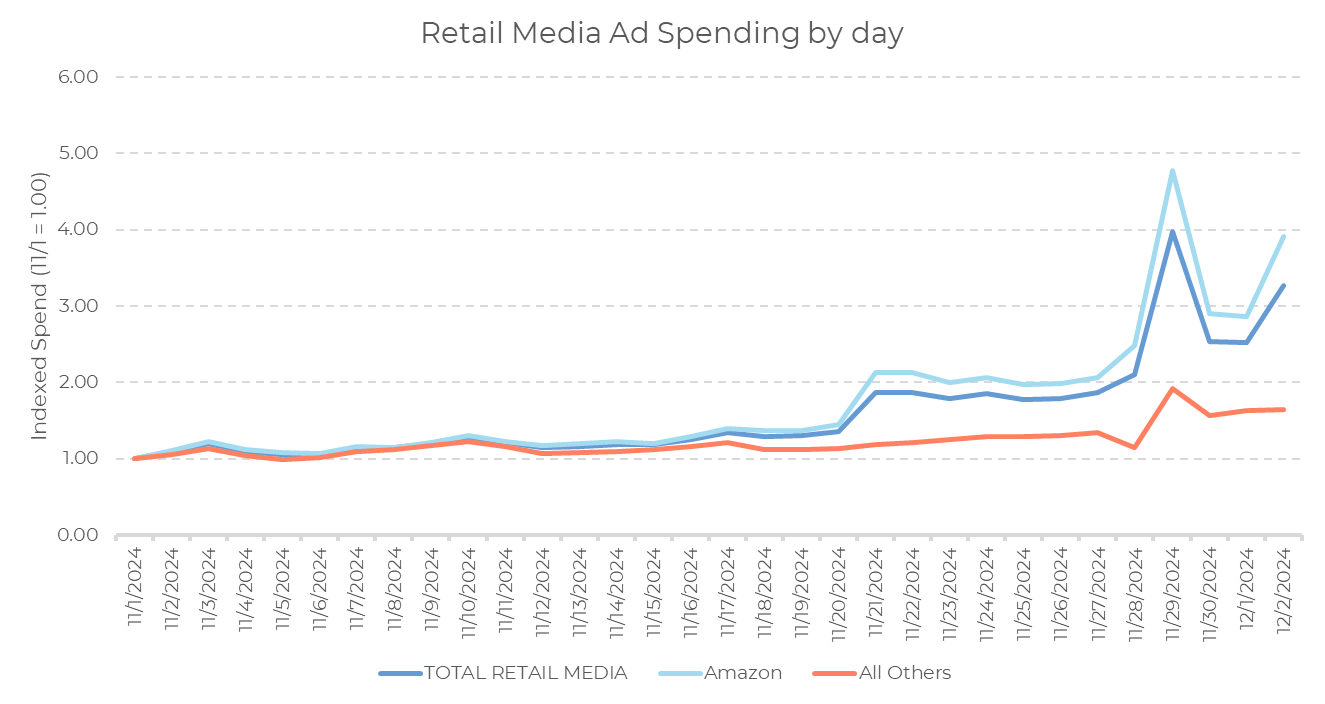

Cyber Monday may have made history as the largest online shopping day in U.S. history, but Black Friday emerged as the stronger day for retail media campaigns. With a clear peak in ad spending, Black Friday continues to be the cornerstone of retail media strategies, offering unmatched opportunities for driving conversion value and capturing consumer demand.

Amazon led the charge as expected, commanding the largest share of retail media budgets. The platform’s spending spiked sharply on both Black Friday and Cyber Monday, reinforcing its position as the go-to channel for retail advertisers during peak shopping days. While other major retail media players like Walmart, Target, and Instacart saw moderate gains, it remains clear that Amazon continues to capture the lion’s share of attention and investment during these key periods.

Retail media spending didn’t fade after Cyber Monday, particularly on Amazon. Elevated spending in the days following the Cyber Five suggests that advertisers are extending their campaigns to maintain momentum. This strategic move likely reflects ongoing demand from consumers looking for deals throughout the holiday season, not just on the peak shopping days.

For marketers, the takeaway is clear: Black Friday dominates the retail media landscape and deserves top priority for campaign planning. However, the sustained activity across Cyber Monday and beyond underscores the importance of a full-season strategy to fully capture holiday demand.

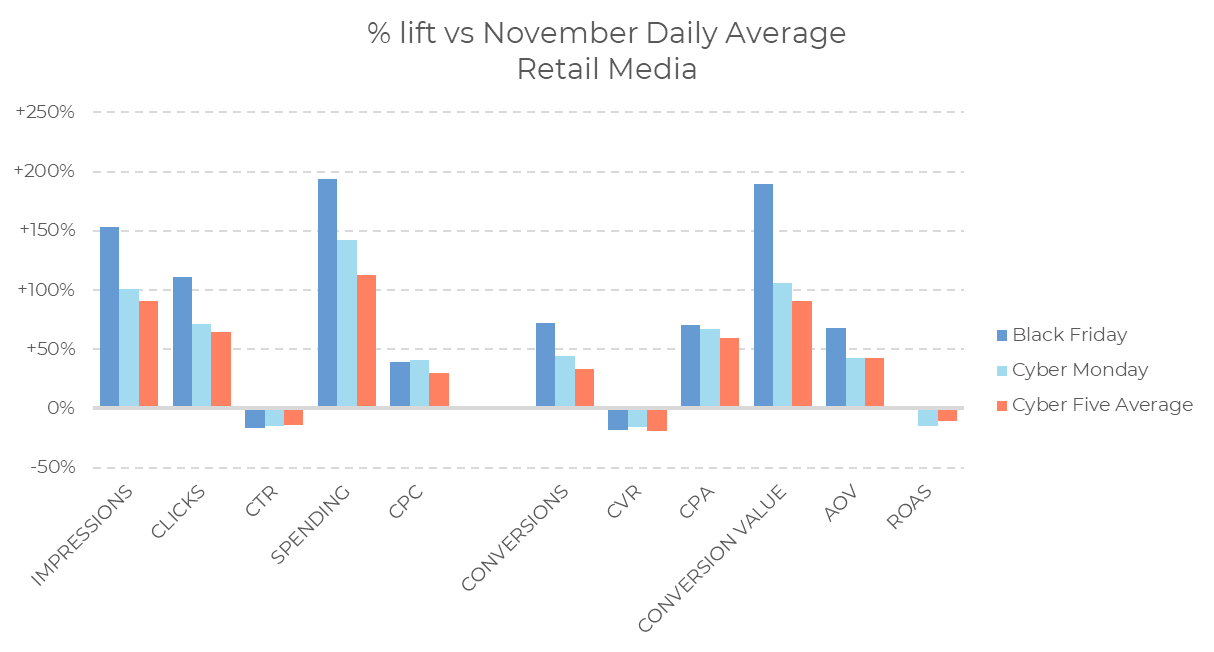

Black Friday dominated retail media performance across most metrics, with the standout being conversion value, where it delivered nearly double the lift of Cyber Monday. This makes Black Friday the most impactful day for retail media campaigns, especially in gift-heavy categories like electronics. While Cyber Monday held its own, its metrics generally trailed behind Friday, except for CPC, where Cyber Monday saw a slightly higher lift (+41% vs. +39%). This suggests advertisers were more aggressive in their bidding strategies on Monday to capture last-minute holiday demand.

Despite Black Friday’s clear lead, Cyber Monday remains a critical follow-up opportunity, particularly as latent conversions may still boost its numbers. For marketers, investing in both days allows for a balanced approach: leveraging Black Friday for broad conversion gains and using Cyber Monday to capture late-stage shoppers willing to pay higher prices to secure deals.

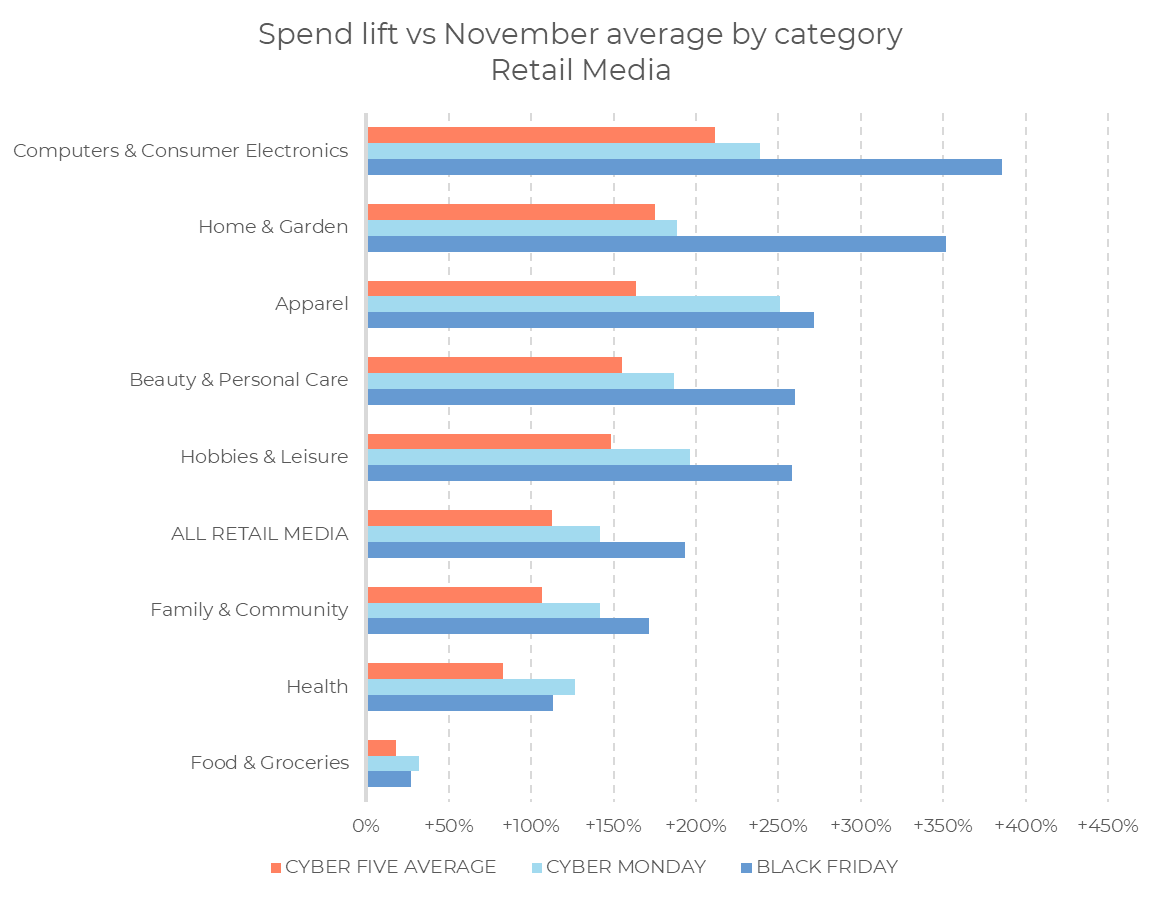

Black Friday led retail media performance across most categories, with Computers & Consumer Electronics seeing the highest lift in spend at nearly 393% above the November daily average. This dominance reflects Black Friday’s continued focus on high-value, giftable items as a primary driver of holiday shopping. Home & Garden also performed exceptionally well, with a lift of 351%, as consumers prepared their homes for seasonal gatherings and decor.

Cyber Monday, while trailing in most areas, came close to matching Black Friday in Apparel, with a lift of 251% compared to 272% on Black Friday. This demonstrates Cyber Monday’s strength in categories that cater to personal purchases and wardrobe updates. Cyber Monday slightly outperformed Black Friday in less gift-oriented categories, such as Health and Food & Groceries, with lifts of 127% and 32%, respectively. While these categories saw more modest increases overall, they highlight opportunities to tailor campaigns to Cyber Monday’s unique shopping behaviors.

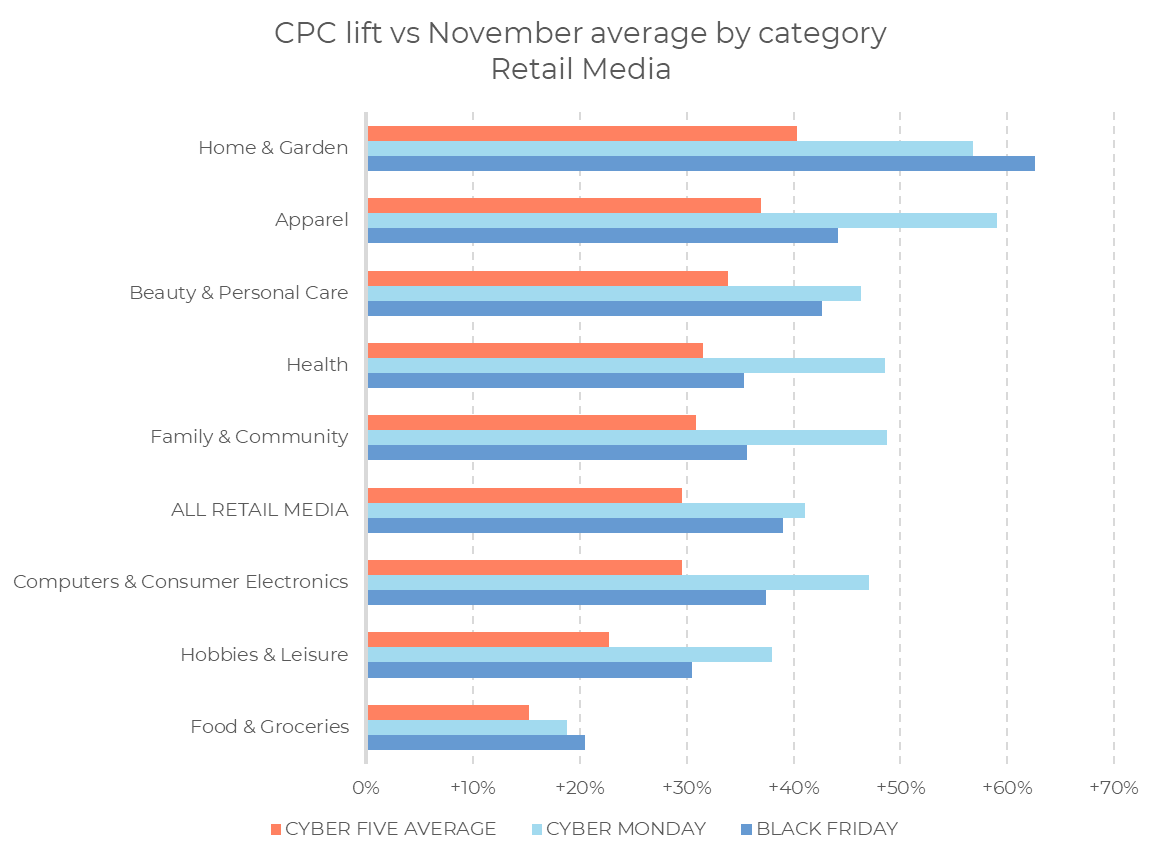

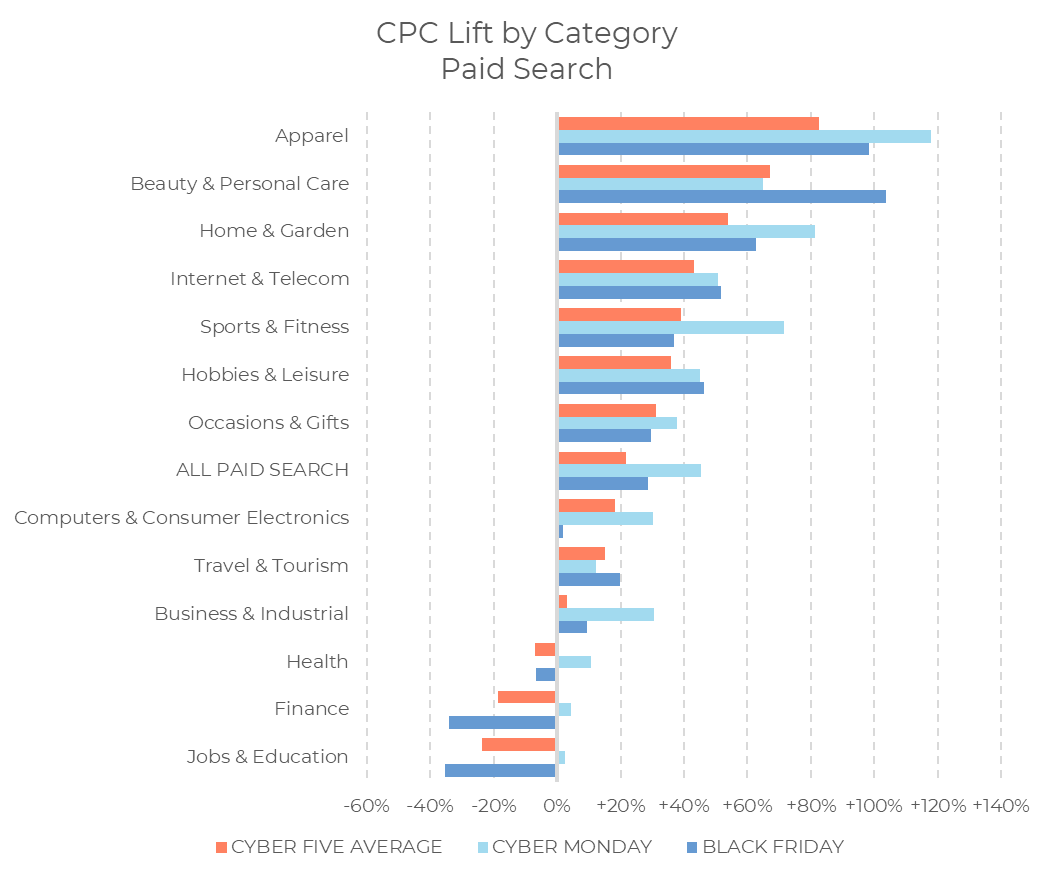

Ad pricing at the category level during the Cyber Five period tells the real, nuanced story. Home & Garden saw the largest CPC premium across all five days, with Black Friday in particular standing out at a 63% lift above the November daily average. This reflects the competitive intensity for seasonal home-related items, where advertisers pushed bids to secure top positions.

Cyber Monday, however, commanded higher CPCs across most other categories. Apparel, in particular, saw a 15-point jump in CPC on Cyber Monday compared to Black Friday, aligning with its spending spike on the same day. Similarly, categories like Beauty & Personal Care and Health also showed elevated Cyber Monday CPCs, signaling that advertisers leaned heavily into bids to capture late-stage shoppers in these segments.

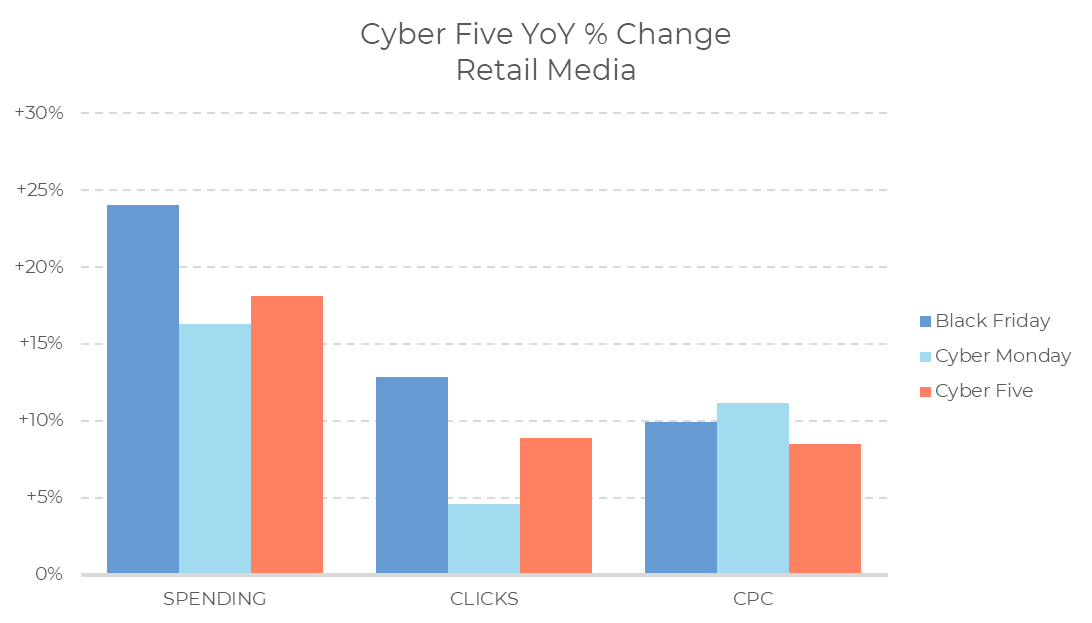

Year-over-year growth in retail media spending during the Cyber Five period was strong, with total spending increasing by 18% compared to the previous year. This growth was driven by a balanced contribution from both click volume and CPC increases, showing that advertisers leaned into both heightened demand and competitive bidding strategies to secure visibility.

Cyber Monday stood out in this regard, with CPC playing a slightly larger role in its spending growth compared to other days. This reflects the day’s focus on capturing late-stage shoppers who were more intent on purchasing, making higher bids worthwhile to win these conversions. Black Friday, by contrast, showed a more balanced mix of click volume and CPC-driven growth, aligning with its broader appeal across multiple categories.

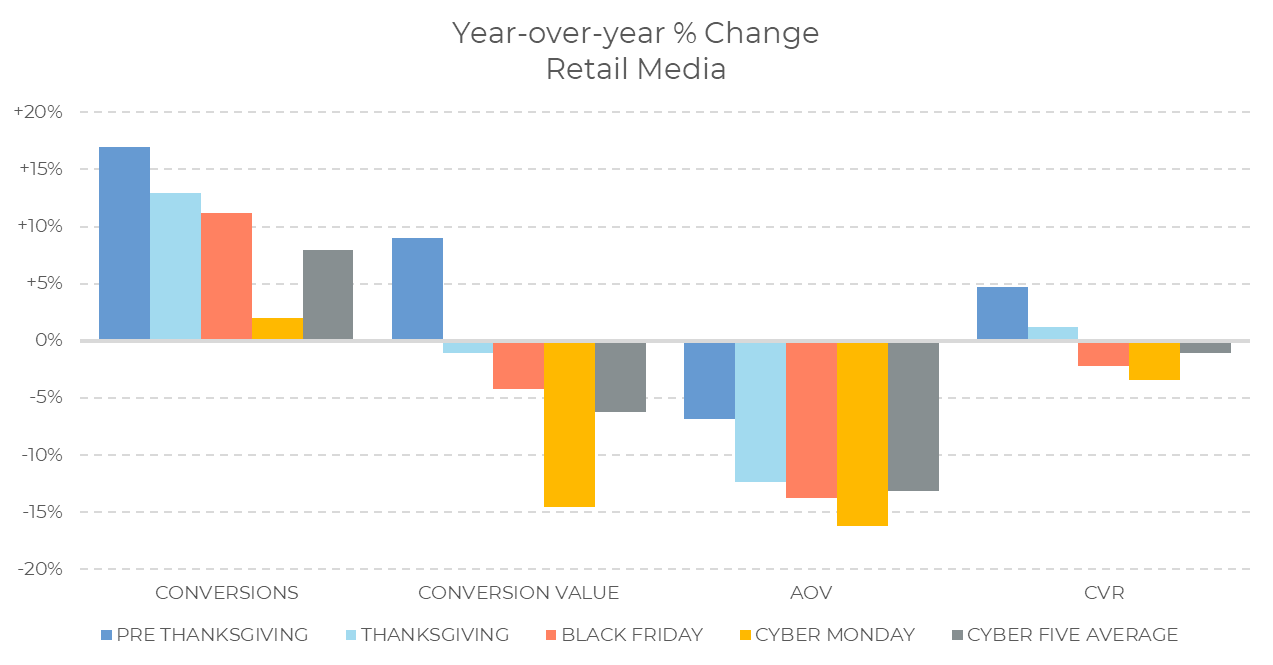

A more complex picture emerges when looking at year-over-year (YOY) conversion metrics. While total sales volumes during the Cyber Five 2024 were slightly down compared to the prior year, pre-Thanksgiving activity significantly lifted conversions and conversion values. This indicates that shoppers started their holiday buying earlier, leveraging early deals and spreading their spending across a longer timeframe.

Despite the decline in average daily sales volumes during the Cyber Five, the longer sales window may offset this reduction. When considering the 27 days of November leading up to Thanksgiving, total conversions and conversion value could meet or even exceed last year’s performance. Cyber Monday’s latent conversions—those that occur after the initial interaction but within attribution windows—are likely to further boost these results. This underscores the importance of taking a holistic, full-season view when assessing the success of retail media campaigns.

How do you manage day by day shifts in paid search demand during Cyber Five?

- Paid search peaks on Cyber Monday with higher CPC pressure.

- Daily controls matter because intent builds across the weekend.

- Paid search during Cyber Five rewards teams that monitor intraday volatility and reallocate budgets fast. Cyber Monday can exceed Black Friday in spend due to aggressive bidding and late stage intent, so marketers should plan flexible budgets, anticipate CPC spikes by category, and use day by day pacing to protect efficiency.

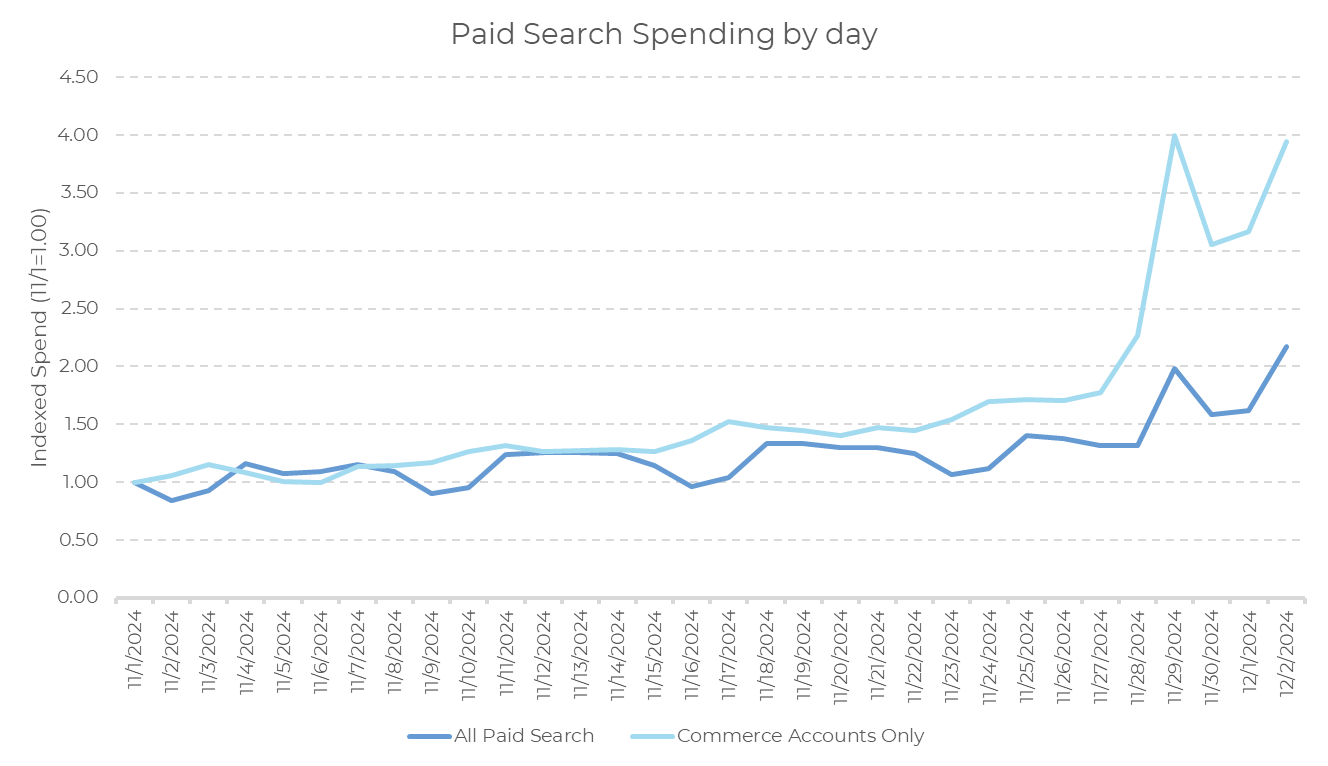

Cyber Monday’s spending on paid search surpassed Black Friday, underscoring the growing importance of this day in the digital marketing landscape. As we see in the data, Cyber Monday’s lift in spending peaked at 3.96x of November 1st’s baseline, just slightly behind Black Friday’s 4.0x peak. While Black Friday remains a key driver of sales, Cyber Monday has solidified its position as the highest spending day of the week for paid search. This aligns with the broader trend of consumers extending their holiday shopping beyond the traditional Friday rush. Marketers who traditionally prioritize Black Friday are now expanding their focus to encompass the full range of the Cyber Five, recognizing that Cyber Monday is becoming just as crucial for driving sales.

The surge in spending on Cyber Monday is a natural extension of the higher-intent traffic that marketers typically see on the day. As consumers finalize their holiday shopping lists, they are more likely to engage with ads from brands that have already established top-of-mind awareness from earlier in the weekend. The data shows a steady increase in paid search spending in the days leading up to Cyber Monday, with a sharp spike on the day itself. This boost in spending, particularly from commerce-focused advertisers, illustrates that Cyber Monday is no longer just a follow-up to Black Friday but a key event in its own right. Advertisers are increasingly shifting budgets to ensure that they maintain visibility across both peak days, optimizing for immediate conversions while also benefiting from the latent conversions that will continue to roll in post-event.

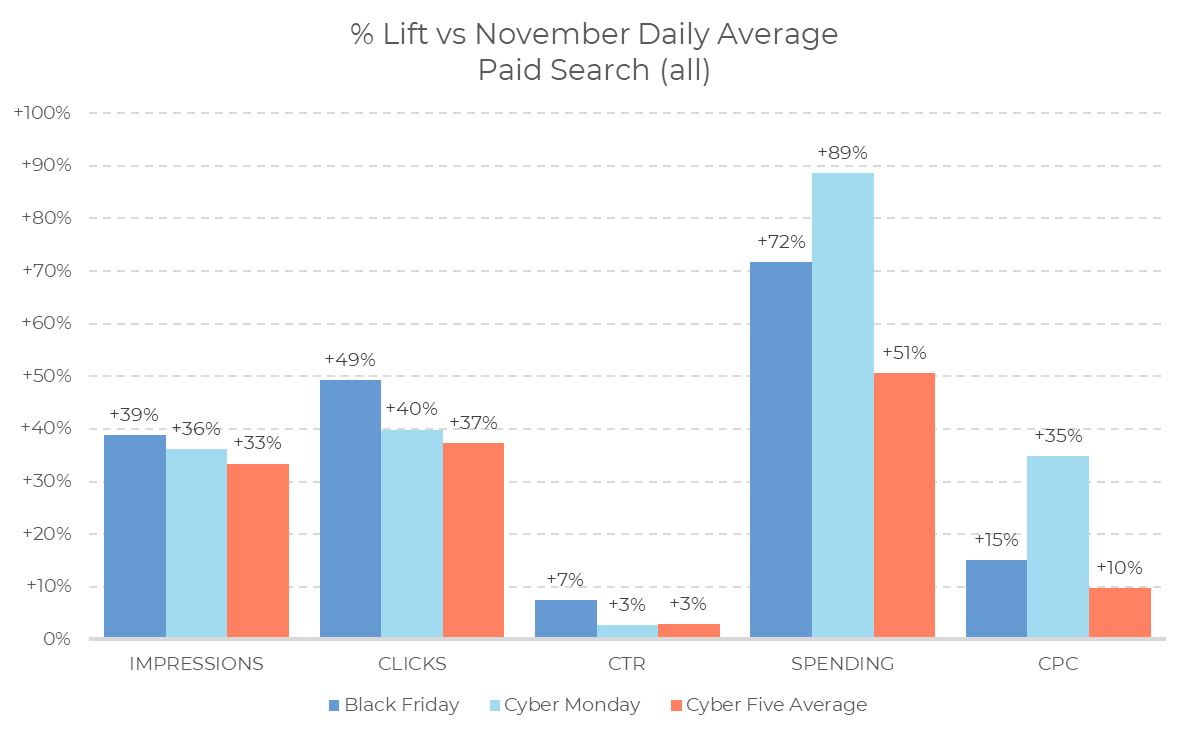

Cyber Monday saw a 72% increase in paid search spending, double the 35% increase on Black Friday. This surge is attributed to higher CPCs, as advertisers bid aggressively to capture late-stage shoppers. While Black Friday still performed strongly with 39% more impressions, Cyber Monday outpaced it in spending and CPC by 35%, reflecting its growing importance for conversions.

Overall, spending during the Cyber Five 2024 increased 51% year-over-year, highlighting the sustained investment across both days. Despite Cyber Monday’s edge in spending, Black Friday remains crucial for early consumer engagement, with both days contributing significantly to overall performance.

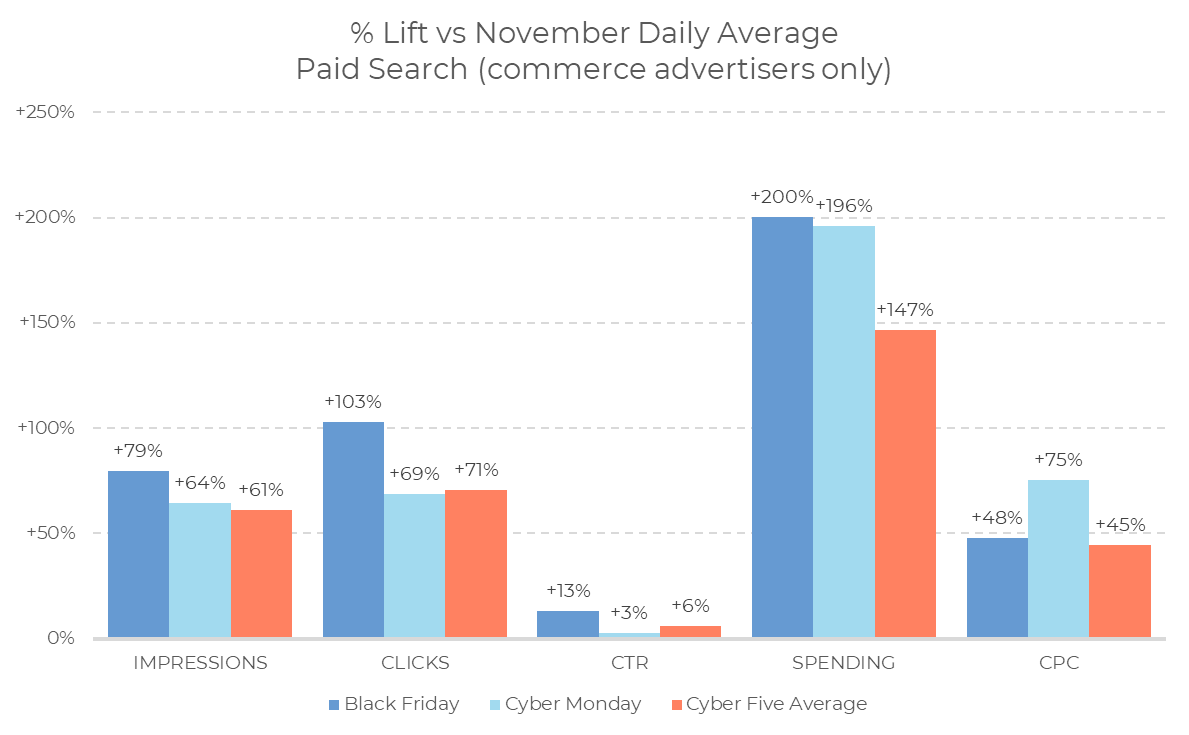

For commerce-focused advertisers, the disparity between Black Friday and Cyber Monday in CPC spikes was similar to the overall trends. Cyber Monday saw a 48% increase in CPC, compared to 75% on Black Friday. However, the key difference lies in the volume of impressions and clicks. Black Friday outperformed Cyber Monday in both areas, with impressions up 79% compared to 64% on Cyber Monday, and clicks seeing a 103% increase, much higher than the 69% rise on Cyber Monday.

Despite the higher CPCs on Cyber Monday, Black Friday’s greater volume of impressions and clicks helped push overall spending to 200% of the November baseline, compared to 196% on Cyber Monday. This suggests that while Cyber Monday was still a strong day, Black Friday’s higher engagement across multiple metrics was the main driver of paid search performance for commerce advertisers during the Cyber Five period.

For commerce-focused advertisers, the disparity between Black Friday and Cyber Monday in CPC spikes was similar to the overall trends. Cyber Monday saw a 48% increase in CPC, compared to 75% on Black Friday. However, the key difference lies in the volume of impressions and clicks. Black Friday outperformed Cyber Monday in both areas, with impressions up 79% compared to 64% on Cyber Monday, and clicks seeing a 103% increase, much higher than the 69% rise on Cyber Monday.

Despite the higher CPCs on Cyber Monday, Black Friday’s greater volume of impressions and clicks helped push overall spending to 200% of the November baseline, compared to 196% on Cyber Monday. This suggests that while Cyber Monday was still a strong day, Black Friday’s higher engagement across multiple metrics was the main driver of paid search performance for commerce advertisers during the Cyber Five period.

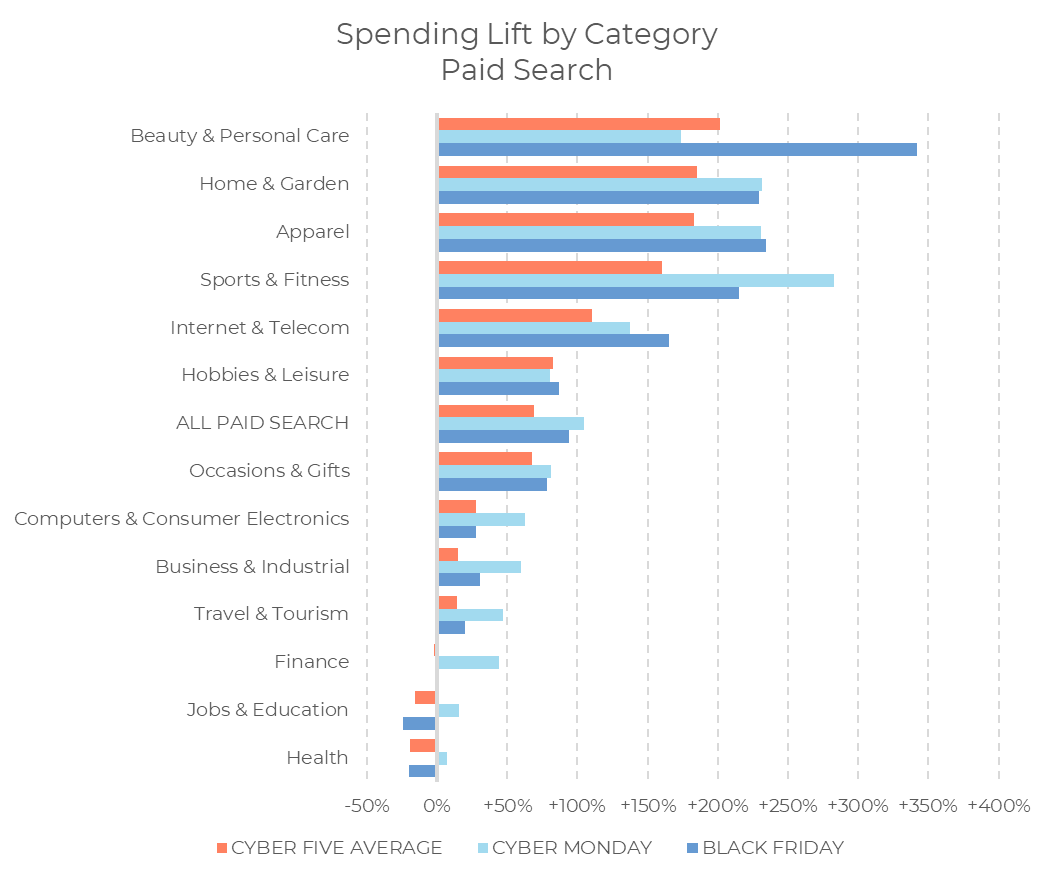

Pricing increases during the Cyber Five period varied significantly across categories, with some showing notable differences between Black Friday and Cyber Monday. Apparel and Beauty & Personal Care saw the largest CPC premiums, with Black Friday seeing higher pricing in both categories. This aligns with the heightened demand for gifts in these sectors, driving advertisers to bid more aggressively to secure visibility on the most competitive shopping days.

For categories like Sports & Fitness, Hobbies & Leisure, and Home & Garden, the pricing trend was more balanced, with both days seeing similar CPC lifts. This indicates that while there was a spike in CPC across the board, certain categories saw more intense bidding on specific days. Marketers in high-demand sectors like Apparel and Beauty need to anticipate these fluctuations and adjust bids accordingly to remain competitive during the Cyber Five.

Why is TikTok emerging as a key paid social player during Cyber Five?

- Platform mechanics differ: Meta leans on CPM, TikTok scales impressions.

- Holiday social success depends on matching creative and auction dynamics.

- Paid social performance during Cyber Five is not one size fits all. Meta can drive results via higher priced inventory while TikTok can expand reach through impression growth, implying different creative, targeting, and measurement approaches. Marketers should align budgets to each platform’s strengths and time their pushes to when engagement accelerates.

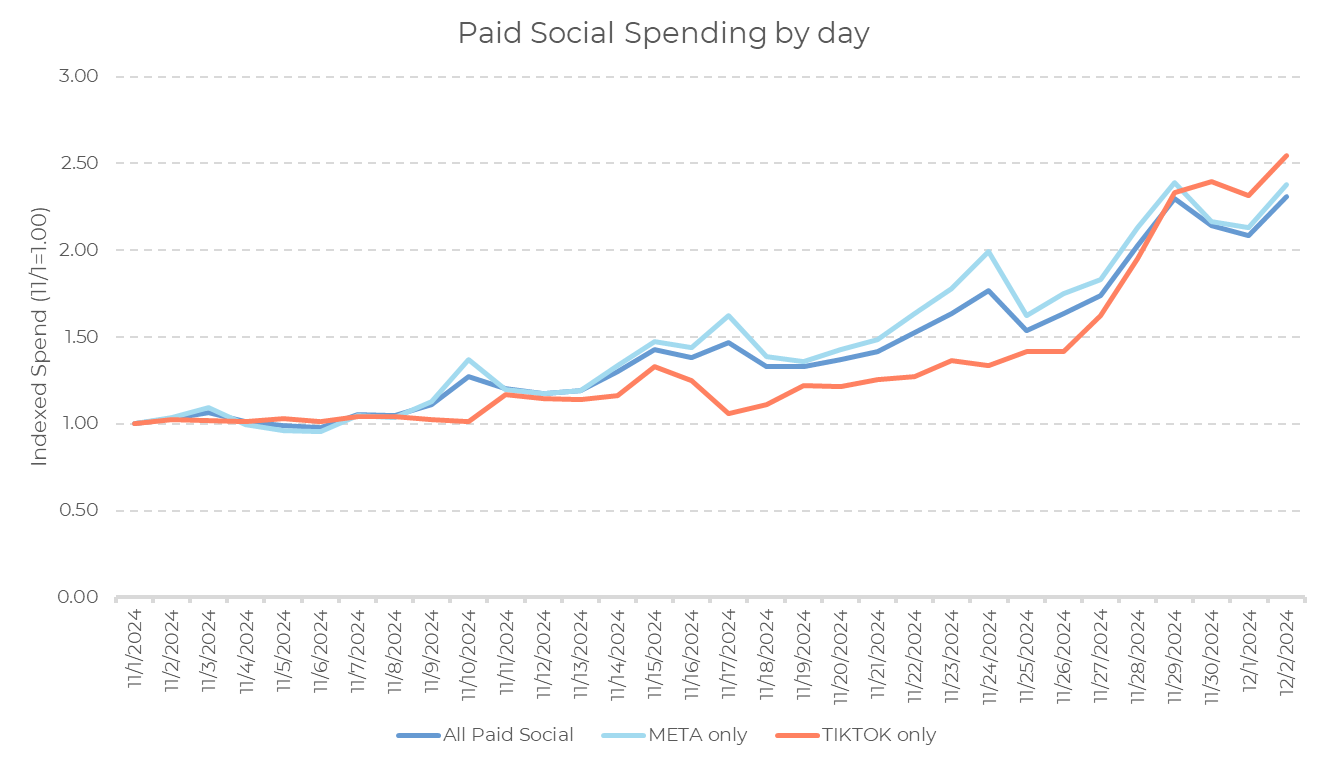

Paid social spending saw a more gradual buildup in comparison to paid search, with noticeable spikes occurring on Black Friday and Cyber Monday, especially for Meta and overall spending. Meta experienced steady growth leading into the Cyber Five period, with spending reaching its peak on Cyber Monday, where it surged to 2.5x the baseline. This growth reflects Meta’s established role in driving both awareness and conversions during key shopping days. While there were spikes during the Cyber Five, Meta’s spending growth was largely steady, with a consistent increase across the weekend, especially on Black Friday, which saw significant engagement.

TikTok, by contrast, displayed a different pattern, with spending picking up more gradually starting the week of Thanksgiving and continuing through the weekend. Its growth accelerated as consumers engaged with the platform in search of deals, but it didn’t see the immediate surge in spending that Meta experienced. TikTok’s performance indicates that the platform may be gaining traction later in the holiday shopping period, catering to a younger audience seeking more organic, influencer-driven content. This trend highlights the distinct behavior of each platform during key shopping moments, with Meta seeing immediate returns and TikTok catching up as the holiday season progresses.

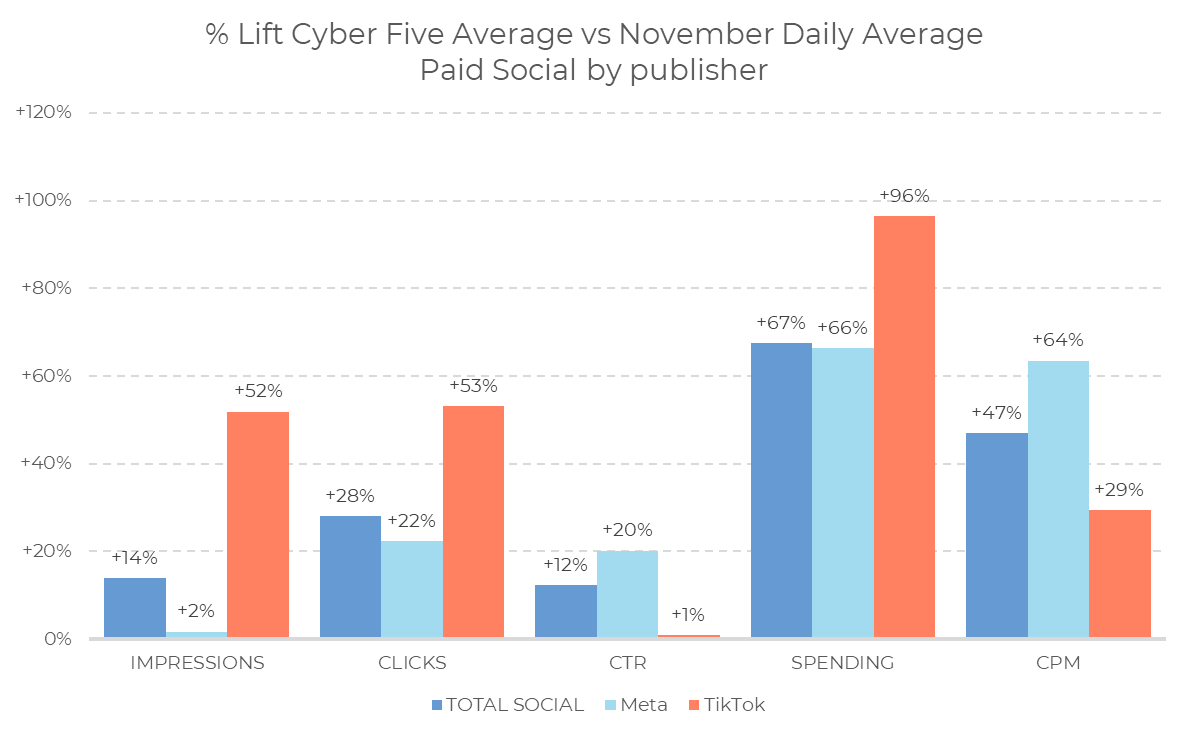

Both Meta and TikTok saw strong growth during the Cyber Five period, reaching 2.3x to 2.5x of November 1st spending. However, the growth paths differed. Meta achieved most of its increase through higher CPM, with impressions up only 2%. This indicates Meta focused on more expensive ad placements to boost results during peak shopping days.

In contrast, TikTok saw a 52% increase in impressions and only a 29% rise in CPM. This shift highlights TikTok’s strategy of expanding reach through more impressions, while Meta relied on higher pricing. TikTok’s growth resembles early Facebook holiday trends, where impressions increased without significant price hikes.

How can marketers glean lasting value from the Cyber Five?

- Cyber Five data reveals category and touchpoint patterns you can reuse.

- Use peak learnings to reshape targeting and product launch visibility.

- The post event value of Cyber Five is not limited to immediate sales. The period compresses consumer intent and competitive bidding into a short window, exposing which categories convert with fewer touchpoints, which respond to timing shifts, and whether new products gain traction. Apply these signals to optimize Q4 and inform year round planning.

The Cyber Five period has once again proven to be a critical time for digital advertising, revealing key trends in consumer behavior and spending. With brands spending more per day during this intense period than at any other time of the year, the data offers a rare glimpse into the dynamics of high-volume spending. While the gift-giving surge drives elevated conversions, marketers can uncover deeper insights into how products, categories, and touchpoints perform under these unique conditions. These insights will guide more effective strategies as we move beyond the holiday season.

For brands looking to optimize future campaigns, the Cyber Five period has shown that certain products, particularly in Beauty & Personal Care and Apparel, require fewer touchpoints to convert, likely due to high consumer demand and purchase intent. These products benefited from early exposure and aggressive bidding, leading to stronger results with less consumer interaction. In contrast, categories like Sports & Fitness saw a boost on Cyber Monday, showing the value of strategic timing and targeting. Marketers should consider the role of timing and purchase intent in shaping their campaigns, using data from these peak periods to refine their targeting strategies moving forward.

Additionally, brands should assess whether their new products were able to catch consumers’ attention during these key periods. As seen with the CPC increases and spend lift across categories, there is a direct correlation between aggressive bidding and visibility. Did your new products stand out? It may be time to increase focus on top-of-mind awareness in future campaigns, as consumers are more likely to engage with ads for products they’ve been exposed to during these high-traffic periods. Optimizing your campaigns based on this data will help you build stronger, more informed strategies throughout the year.

Methodology: Our analysis focuses on the performance data from Skai clients during the 2024 Cyber Five period, spanning Thanksgiving (November 28) to Cyber Monday (December 2). We also examine trends from the pre-Cyber Five period, from November 1 to November 27, to understand how early holiday activity influenced the peak days. Data analyzed includes retail media, paid search, and paid social spending, impressions, clicks, conversions, and cost-per-click (CPC) variations.

Related Reading

- Men’s Retail Holding Company increases conversions and revenue over 100% with Skai powered Smart Bidding Shows how search automation can protect efficiency when CPC pressure rises during peak demand.

- Enhancing Amazon Ads Efficiency: OMD Elevates Philips’ ROAS by 8% through Skai’s Budget and Dayparting Capabilities Demonstrates how dayparting and budget pacing help sustain performance when spend spikes across tentpole shopping days.

- Skai’s Impact Navigator helps Privalia have more confidence in their audience strategies Highlights a measurement driven approach to validating where incremental value is coming from before reallocating budgets.

Frequently Asked Questions

What is Cyber Five 2024 and why does it matter for advertisers?

Cyber Five 2024 is the five day window from Thanksgiving through Cyber Monday when online demand and ad auctions peak. It matters because intent compresses into a short period, CPC and CPM can spike, and retail media, search, and social each behave differently by day. Planning for both peaks and post event momentum improves total season results.

How should I split budgets across retail media, paid search, and paid social during Cyber Five?

Start with retail media to capture high intent shoppers where they buy, keep paid search flexible to follow day by day demand shifts, and use paid social to build and refresh audiences before and during the weekend. Set guardrails for pacing and profitability, then reallocate daily based on conversion value, CPC pressure, and inventory availability.

Why do CPC spikes differ between Black Friday and Cyber Monday?

CPC spikes differ because competition, inventory, and shopper intent shift by day and by category. Black Friday often brings broader browsing volume and heavy gifting pressure, while Cyber Monday can concentrate late stage buyers who are closer to purchase. Anticipate category specific bidding surges and pre set bid and budget rules so you can respond fast.

How do I decide whether to invest more in TikTok or Meta for holiday social?

Decide based on how each platform is delivering your results. If you need efficient reach expansion and creative discovery, prioritize the platform where impressions scale without runaway pricing. If you need stable conversion support with proven audiences, prioritize the platform where retargeting and measurement are strongest. Test both with clear creative and audience splits, then shift budget to the winner by KPI.

What should I do after Cyber Five to capture latent conversions and learnings?

Keep a controlled level of spend immediately after Cyber Monday to capture late converters and deal seekers, then analyze which products converted with fewer touchpoints and which needed longer journeys. Build retargeting audiences from peak traffic, refresh creative with best performing value props, and document category timing patterns to inform the rest of Q4 and early Q1 planning.

Glossary

Cyber Five: The five day shopping period from Thanksgiving through Cyber Monday.

Retail media: Advertising placements sold by retailers that use shopper data and onsite or offsite inventory to influence purchase.

Cost per click CPC: The amount an advertiser pays for each click on an ad.

Cost per mille CPM: The amount an advertiser pays per thousand ad impressions.

Latent conversions: Purchases that occur after an ad interaction within the attribution window rather than immediately.

Social commerce: Shopping behavior and purchases that happen within or are strongly driven by social platforms and creator content.

More like this

-

2026 CPG Marketing Formula #5: Operational Strength Is Your Competitive Advantage

-

2026 CPG Marketing Formula #4: Preparing for Agentic Commerce

-

Retail Media in 2026: Predictions From Industry Leaders

-

2026 CPG Marketing Formula #3: Building Always-On Incrementality

-

Retail Media in 2026: Predictions from Skai Experts

-

Cyber 5 2025: A Huge Week for Consumers and Commerce Media