Skai recently released our Q3 2015 Digital Marketing Snapshot summarizing global trends in Paid Search and Paid Social advertising and Regional Paid Search Trends in the Americas, EMEA and APJ regions.

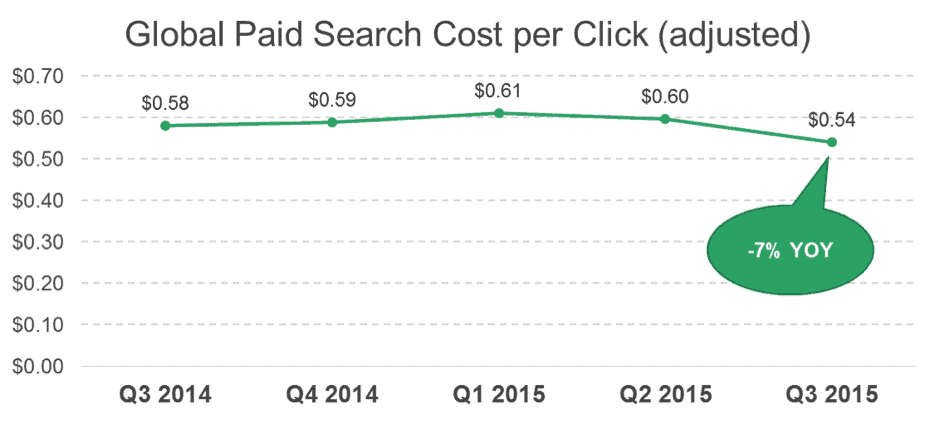

One finding that has jumped out at many people who have considered these reports is that we have seen a -7% year-over-year drop in CPC, from $0.58 to $0.54 when adjusted for currency fluctuations.

By comparison, Google recently released quarterly results where they described a similar drop of -11% versus Q3 of 2014. Several other outlets, however, have reported year-over-year increases in search CPC.

So what’s going on here? You would think that both findings can’t be right, but I am going to argue that’s exactly what is happening.

To reconcile the differences between data that shows a CPC decrease versus data that shows an increase, it’s important that marketers pay attention to the methodology around any trend data.

The Google and Skai numbers include either all advertisers, or nearly all advertisers. On the other hand, many analyses only include advertisers who have spent consistently over the period of the analysis, akin to how retailers and other chains measure “same store” sales. While this does a good job of tracking changes made by longer-tenured advertisers, it has the potential to miss any changing demographics from new entrants to paid search advertising.

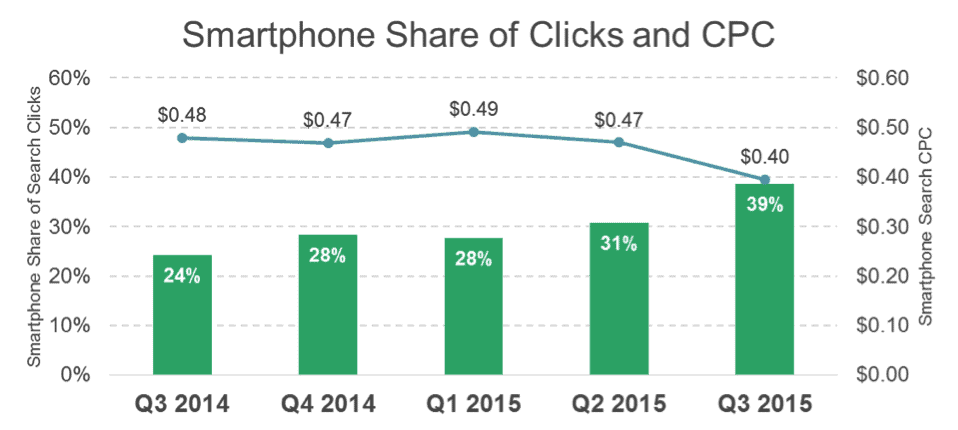

For example, there is a consensus of opinion that one driving factor in search CPC trends is the role of mobile search. Clicks from mobile devices tend to be less expensive than their desktop (and tablet) counterparts, and are also making up a greater share of the overall click picture. So it stands to reason that overall CPC would be either dropping, or as some of those other reports have indicated, at least growing more slowly than they have in the past.

Now imagine if a startup company that has only been advertising for six months is more heavily invested in mobile than a company that has been advertising for five years. There are probably more than a few advertisers who would fit that bill, right? Not to mention that this “new money” might have other defining characteristics that signal a sort of demographic shift that wouldn’t be captured if 12 to 24 continuous months of spend were required for consideration.

There are pros and cons of both methods of looking at CPC. The same-store approach can shed light on what advertisers with a longer history may be seeing in their search programs. The census approach looks to uncover insights about paid search marketing as a whole. Both are entirely valid and insightful, and the agile marketer has the ability to understand how each of these data points comes to bear on their own experiences.

You can find more data insights in the infographics, and don’t get me started on the relative merits of currency adjustments…