At the end of February, the news broke that Google was making a major change to the search engine results page (SERP) for desktop searches. The sense of chaos was palpable. Would CPCs skyrocket? Would users lose themselves in the now-vacant white space on their screens, contemplating eternity and fractional divisions thereof? What would happen to the “Golden Triangle” from all of those eye-tracking studies?

Well, now we have some data. The sky has not fallen, and CPCs, in fact, have not skyrocketed.

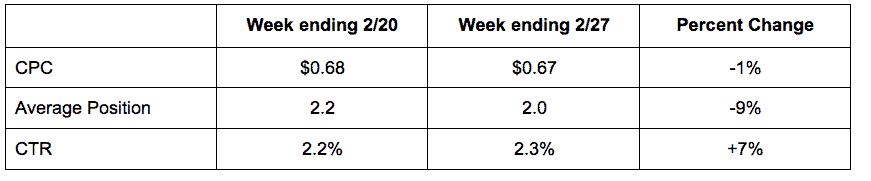

Across the Skai platform, the first week after this change was fully rolled out actually saw a one penny (or roughly 1%) decrease in CPC. The biggest differences we saw were that average position improved by 0.2, moving ads closer to the top of the page on average, and that click-through rate (CTR) increased by one tenth of a percent, which represents a 7% increase over the previous week. Week-over-week changes to click and spend volume were ultimately within normal weekly variance, with a small increase in clicks and a smaller increase in spending due to the drop in average CPC.

The increase in CTR is something many people expected. Impression supply is being constrained, while overall intent has not changed. This is something we saw, in much more drastic fashion, when Facebook changed its focus from its right rail ads to the News Feed.

It’s the CPC and average position movement that is intriguing. Wasn’t this supposed to jack up competition for highly-visible keywords? If anything, you might have expected that any rise in average position would be accompanied by an increase in CPC as bidding strategies kick in to maintain position.

For average position, our team has noted that the smaller number of ads per page can have a material effect on how this metric works in aggregate, as many of the impressions from lower positions simply do not exist to pull the average away from the top. This may simply be an artifact of how the math works on the new layout.

Additionally, what we may be forgetting in all of this is that much of the alarm raised at this change was for individual keywords, while at an advertiser level, we are looking at very large sets of keywords, and those sets can behave much differently.

It may very well be the case that some keywords are fighting harder for their position, but those are counterbalanced by keywords that may be losing that fight, and a bidding algorithm that works across groups of keywords will take all of these different contributions into account.

On balance, we are seeing that the winners are driving the overall performance of the portfolio, delivering better engagement at the same price. So the key becomes not the change itself in many cases, but the (in most cases algorithmic) response to those changes. Is it possible that everybody wins in this scenario?