Q2 2024 saw dynamic shifts in global digital advertising. Skai’s media performance research highlights regional differences: EMEA trails AMER in Amazon Ads spending growth, though the UK outperforms EMEA due to higher conversion rates despite lower CPC. Meanwhile, Google’s paid search shows stronger growth in EMEA, driven by the UK, where clicks are up and CPC remains above the regional average but below AMER. Read more from Skai’s Sr. Director of Media Research, Chris Costello.

The Q2 2024 Quarterly Trends Report covers a lot of ground, but there will always be some analysis that doesn’t make the final cut. In particular, what about regional differences between North America (AMER) and the Europe, Middle East and Africa (EMEA) region? And within EMEA, how did the United Kingdom (UK) perform?

The largest of the walled garden publishers provide the biggest opportunity for this type of geographical analysis, so with that in mind we will focus specifically on Amazon and Google as proxies for the retail media and paid search channels, respectively.

Note: Analysis is based on accounts with fifteen consecutive months of spending at the channel level. Some outliers have been removed. Spending and cost-per-click metrics are calculated in US Dollars and converted to Euros based on the exchange rate on the last day of the quarter (30 June).

Amazon Ads

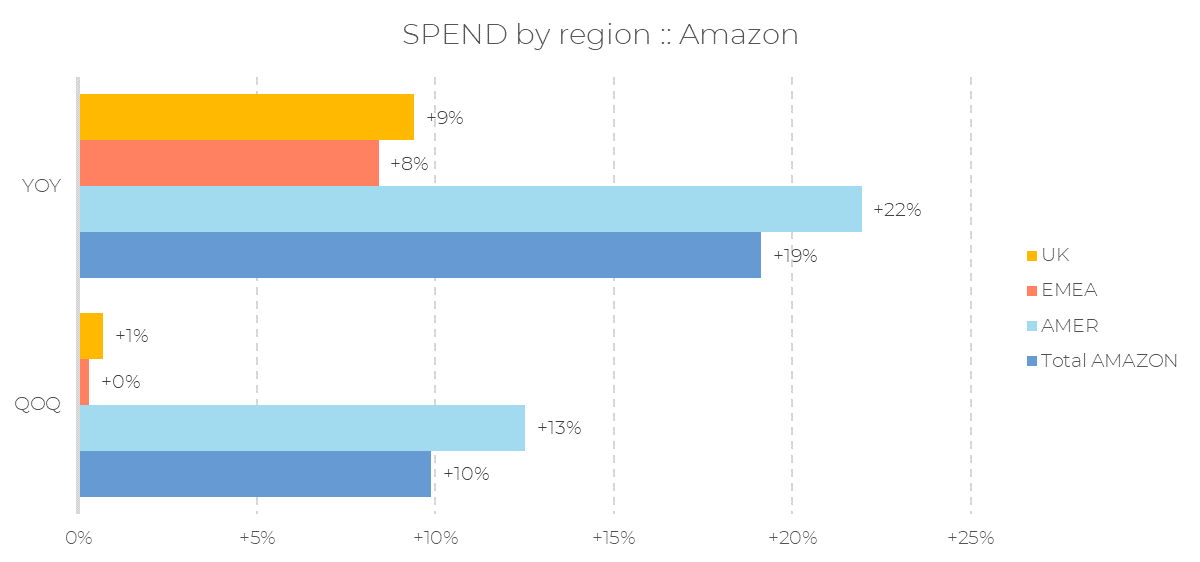

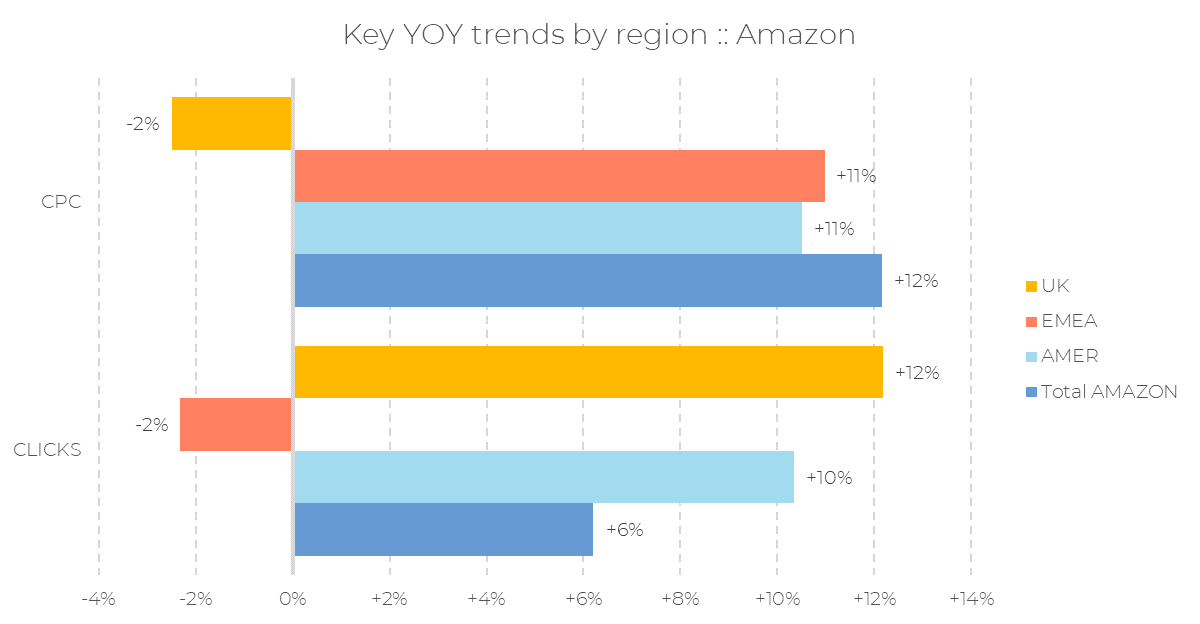

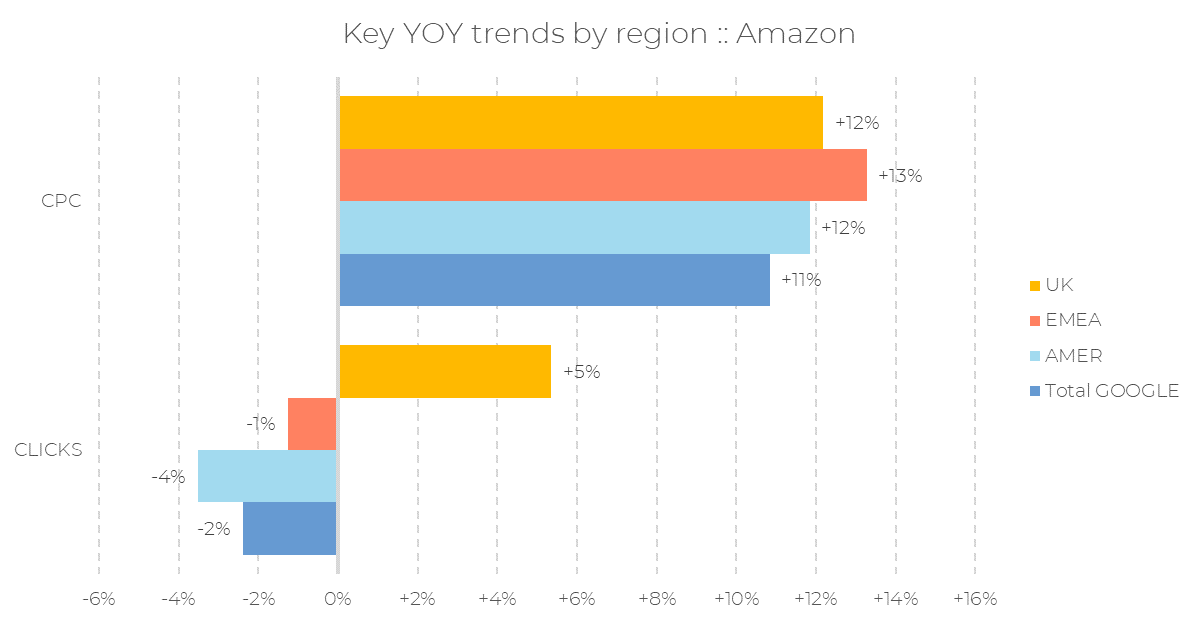

Overall Amazon Ads YoY spending growth in EMEA trails the AMER region, while UK spending growth was one point faster than overall EMEA, which includes the United Kingdom except where noted otherwise. QoQ results were similar, but of smaller magnitude.

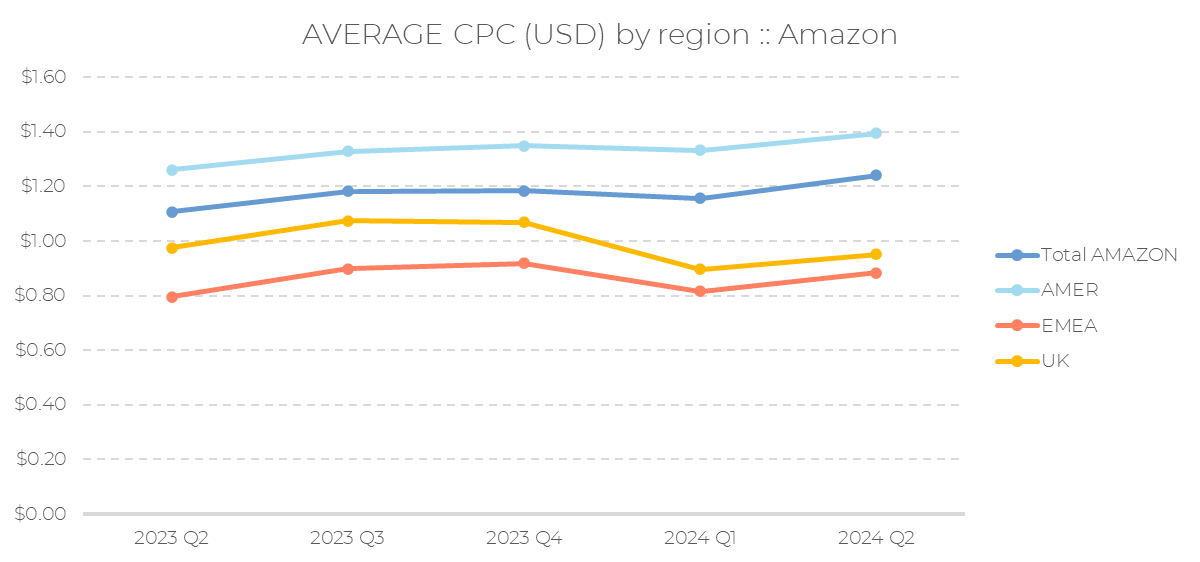

Why might this be the case? One underlying cause for this is that CPC in EMEA (and the UK) is less than that of AMER.

What’s more, CPC in the UK, in particular, dropped YoY. So the UK saw faster click growth but lower CPC. The larger EMEA market saw shrinking clicks with comparable CPC growth to AMER. While the details are slightly different, both of these combinations contributed to slower spending growth for the region, and the country.

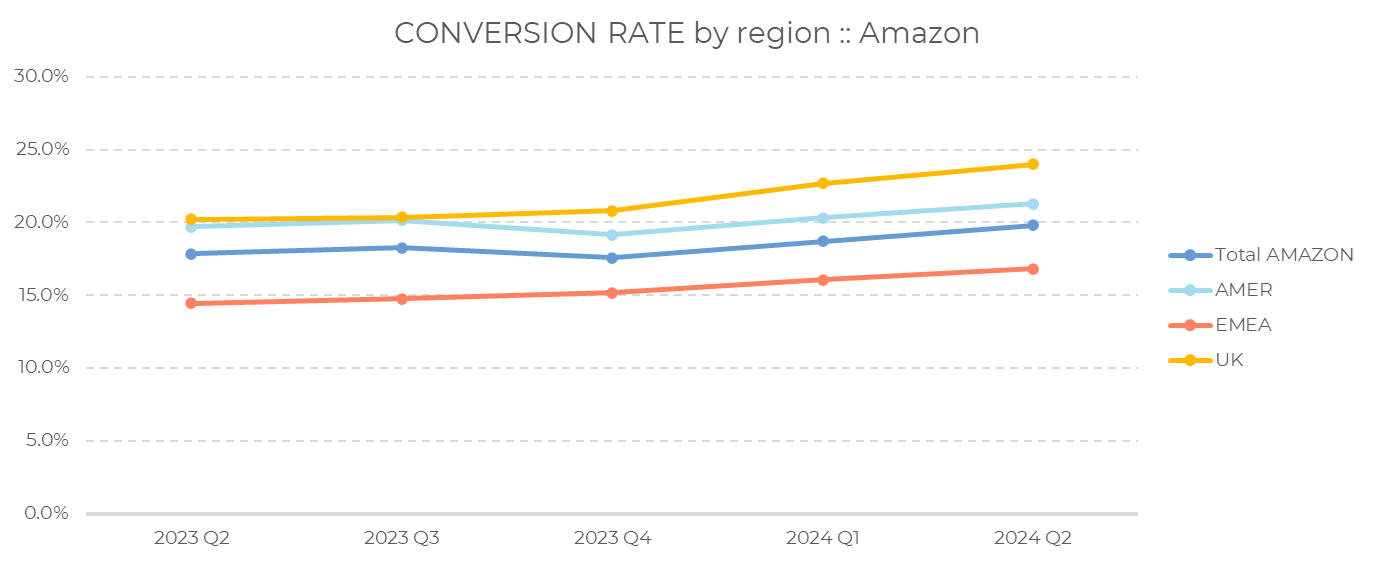

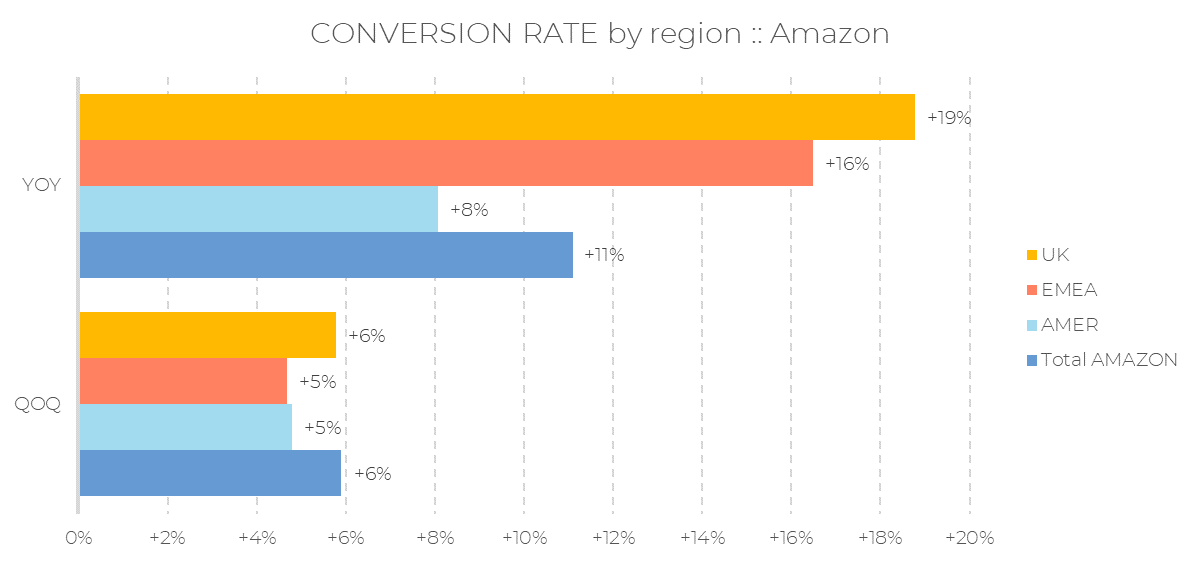

Broadly speaking, we have seen higher conversion rates accompanying higher CPC, likely to be the result of improving economic conditions, narrower audience targeting, a tighter focus on higher-performing campaigns, or some combination of all three. The one exception in our breakouts here is the UK, where CPC went down YoY but conversion rates still increased, and actually increased faster than EMEA, AMER or globally.

The UK also has a higher conversion rate than AMER, EMEA or the global total. The difference between the UK and the rest of EMEA may be as simple as getting what they paid for, as CPCs are consistently higher in that country versus the balance of the region, even when broken out by category. The difference with the AMER region only started manifesting itself in Q4, and may have more to do with the mix of categories and purchase behavior.

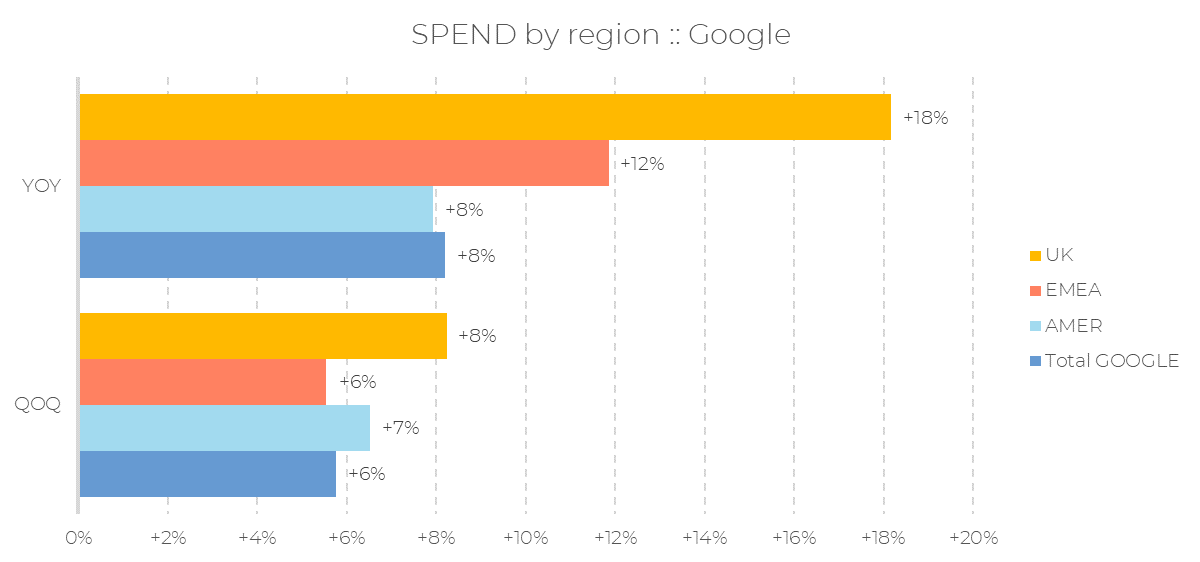

Spending growth in EMEA was faster than AMER, led by the UK at a very robust +18% YoY.

Clicks grew in the UK, and shrank less in EMEA, which was a big contributor to the faster spending growth.

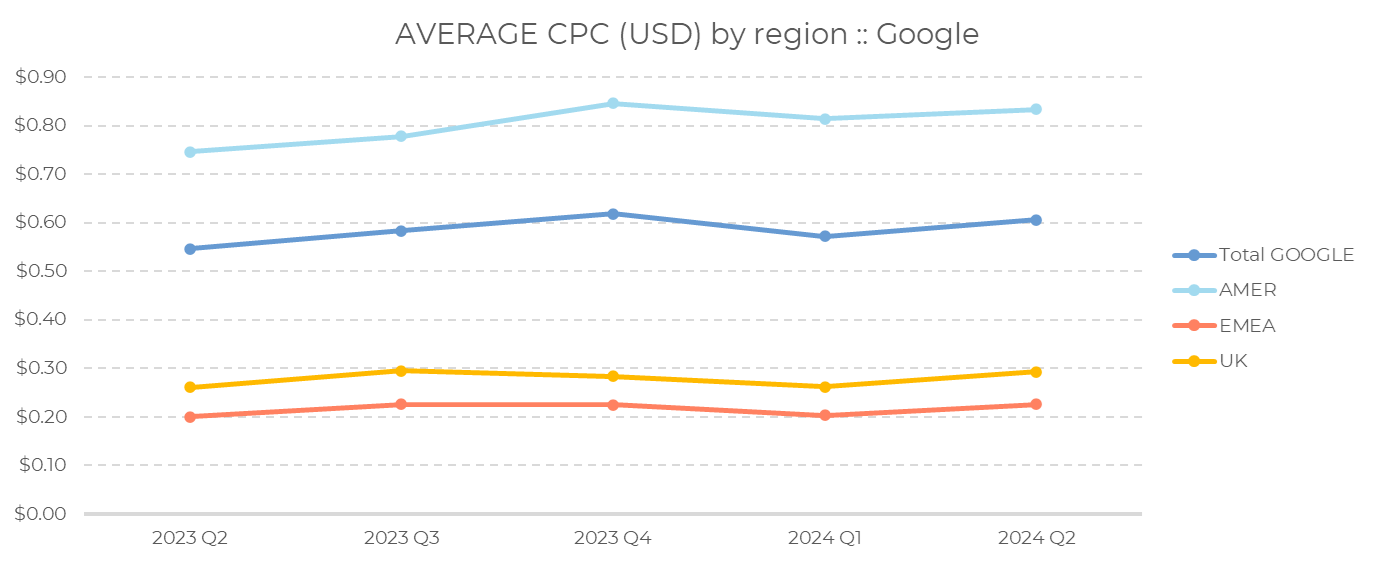

CPC in the UK was higher than the EMEA average, but considerably lower than AMER and the overall average. The difference is largely a combination of category and ad mix. EMEA and the UK both have a heavy footprint from at least one prominent third-party marketplace in the Hobbies & Leisure space that serves a lot of low-priced standard shopping ads. Across the pond, the AMER numbers are bolstered by higher-priced keyword ads from non-retail advertisers who are more focused on lifetime value (LTV) than individual transactions, giving them more headroom to bid up prices of individual ad clicks.

Digital marketing is not monolithic. Not all programs behave in unison, particularly when considering geography. While North American trends tend to dominate the overall picture–especially in our data–looking at geographical differences can help provide valuable context depending on where you, as a marketer, are running your programs.

In retail media, EMEA and the UK are running behind AMER in terms of overall growth. In paid search, it’s the opposite. Both channels have a slightly different calculus when it comes to volume vs. pricing, and these are the types of differences that can help marketers understand how they measure up.

More like this

-

Amazon Prime Day 2026: Record Results Through Smarter, More Efficient Advertising

-

Winning Walmart Deals in 2026: A Three-Phase Walmart Connect and Skai Playbook

-

Walmart Deals 2026: 8 Numbers That Should Shape Your Approach

-

Prime Day 2026 Playbook: From Final Prep to Post-Event Growth

-

Tinkering Is Not Transformation: What Marketing Leaders Need for the Agentic Era

-

Prime Day 2026 Preview: 7 Shifts From 2025 to Guide Your 2026 Playbook