Amazon Prime Day 2024 saw record-breaking sales driven by a 496% increase in global ad spend. Over 200 million items were sold during the 48-hour event, with ad-attributed sales revenue growing by 468%. The event also showed signs of influencing other digital marketing channels, including Google’s search shopping campaigns. Read the post for the entire analysis, including category, ad format, and other Prime Day KPIs.

Once again, Amazon announced record-breaking sales for its latest iteration of Amazon Prime Day, which ran July 16-17, 2024. Over 200 million items were reportedly sold during the 48-hour period!

This, in and of itself, is not surprising. Prime Day has been growing steadily since its inception in 2015. Following suit, the annual sales event didn’t just open up the floodgates of consumer purchasing but also advertising spending by brands and marketers, with global ad spending up 496%, while cost-per-click (CPC) increased 66%. The result: advertising-attributed sales revenue grew by 468%.

When we examine Skai’s Prime Day data, we focus on two things:

- How did Prime Day compare to the daily average for the previous 30 days, both overall and by key segments?

- How did Prime Day compare to July of last year?

In 2024, Amazon DSP was in full force, which added some nuance to some of these questions. It’s always been up for debate whether Prime Day really confers some sort of “halo effect” on other channels, particularly paid search.

First, some ground rules. When we say “Amazon Sponsored ads,” we mean ads on the Amazon site or app, which are broadly defined as Sponsored Products, Sponsored Brands, Sponsored Brand Video, and Sponsored Display. Amazon DSP comprises ads served by Amazon on external properties.

Methodology: Unless otherwise noted, the following short-term lift analysis looks at 32 days of performance across all Skai Amazon accounts globally from June 16, 2024, through July 17, 2024. Year-over-Year (YoY) analysis only includes accounts that spent on Sponsored ads every day of that 32-day period and every day from June 11, 2023, through July 12, 2023.

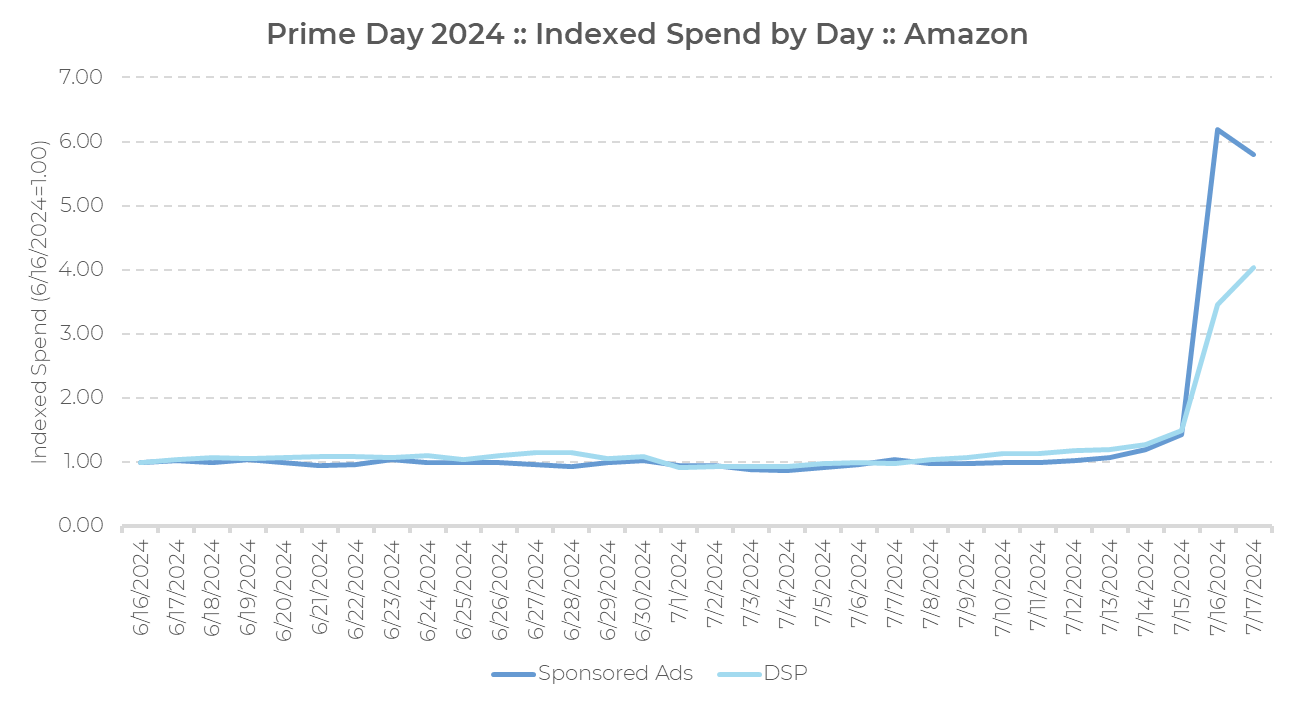

Advertisers shifted where they spent each day

As we have seen for previous Prime Day events, ad spending spikes considerably during the 30 days leading up to the event. We break out Sponsored ads and DSP, but we won’t combine them because we do not know if our relative share from these two buckets is representative of Amazon as a whole.

Note: Spending is indexed, which means the first day of the visualization is set to 1.00, and all subsequent days are indexed relative to that first day. So a value of 2.00 means that the day is 2x of that first day, all the way to the left on the chart.

From this view, we can see that spending on July 16 was about 6x the spending on June 16. DSP spending spiked about half as much as Sponsored ads. Day two spending went down for Sponsored ads and up for DSP. And there was no gradual buildup of spending leading up to Prime Day.

The short-term lift from Prime Day

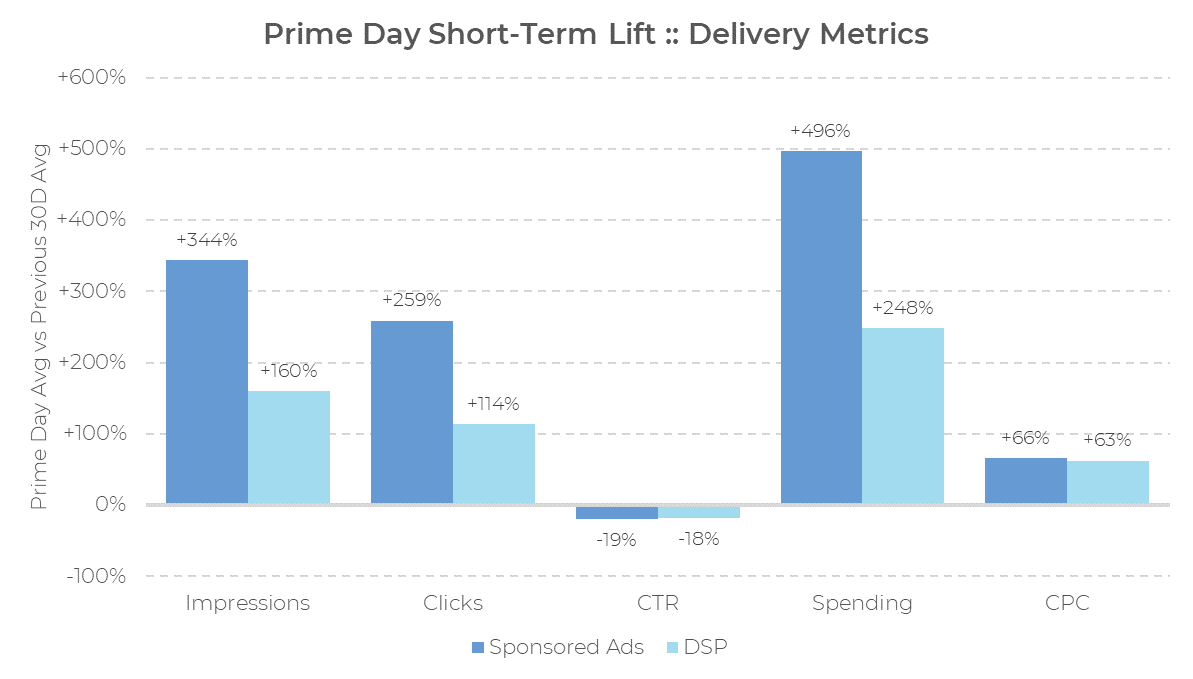

We quantify this type of trend by looking at the short-term lift, which is the average for the two days of Prime Day compared to the average for the 30 days before that. Lift is expressed as a percentage difference. So doubling spending would be the equivalent of +100%. Let’s first look at delivery metrics, which are Impressions, Clicks, and Spending, as well as clickthrough rate (CTR) and average cost per click (CPC).

The average CPC grew about the same for both Sponsored ads and DSP, but Sponsored ads saw roughly double the bump in impressions, clicks, and spending. The average spend across the two days of Prime Day for Sponsored ads was just shy of 6x the daily average from 6/16 through 7/15 (+496%), while DSP spending was up 3.5x (+246%).

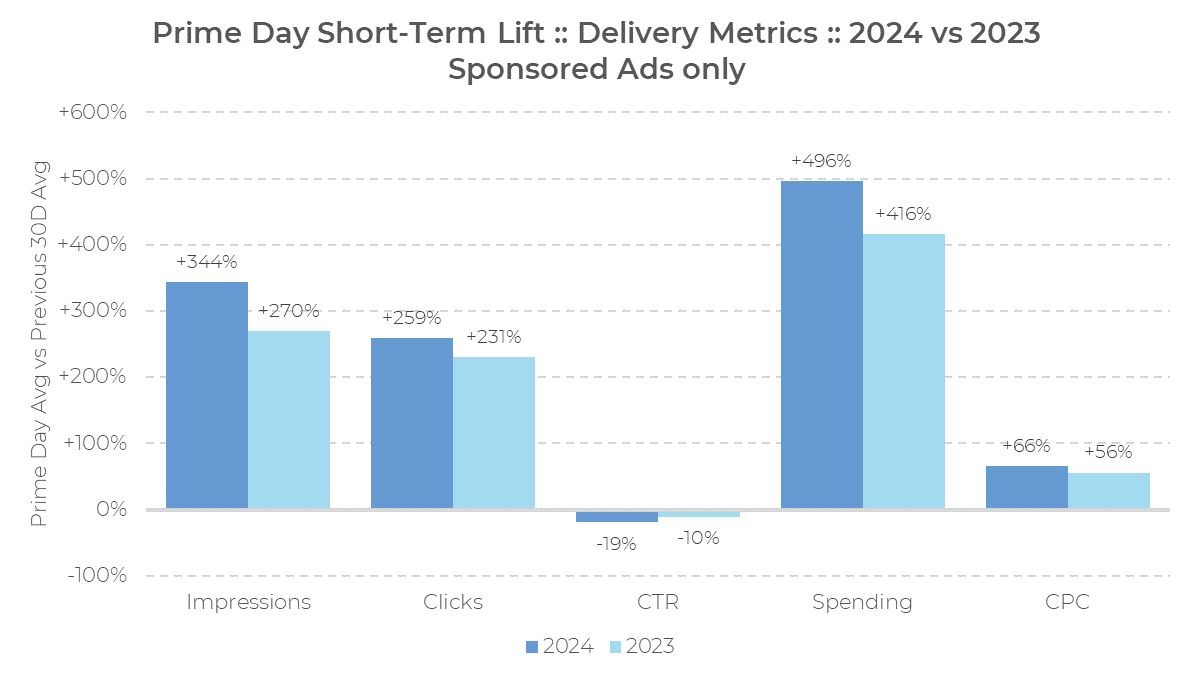

It’s not quite the same as looking at same-store YoY spend, but another way to put these increases into context is to compare them to the same short-term lift from last year. For this analysis, we will consider only Sponsored ads.

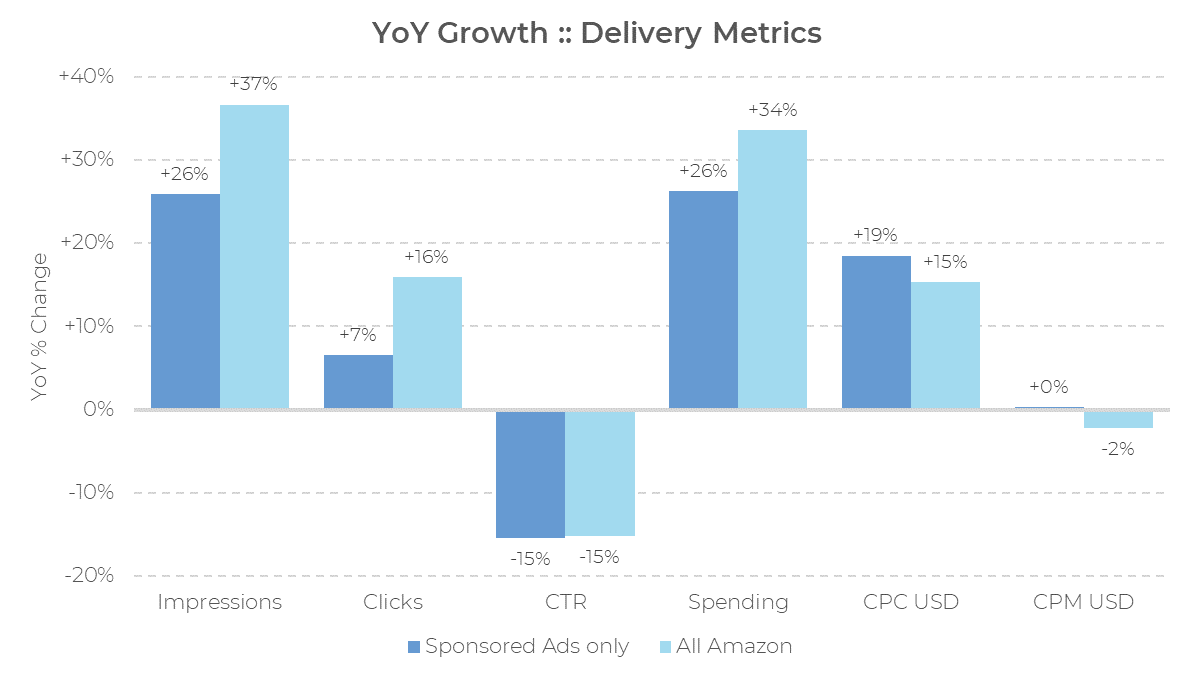

Across all of our metrics, 2024 saw bigger movement than 2023, and a sharper increase in impressions than clicks meant that the CTR drop was bigger as well.

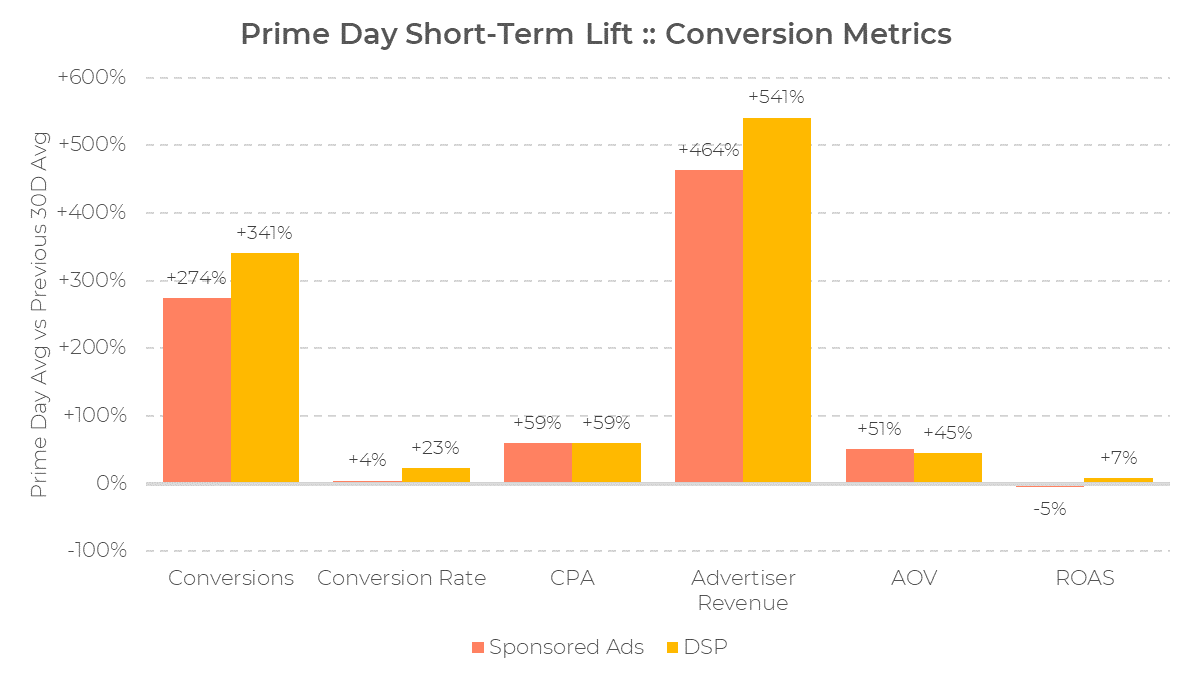

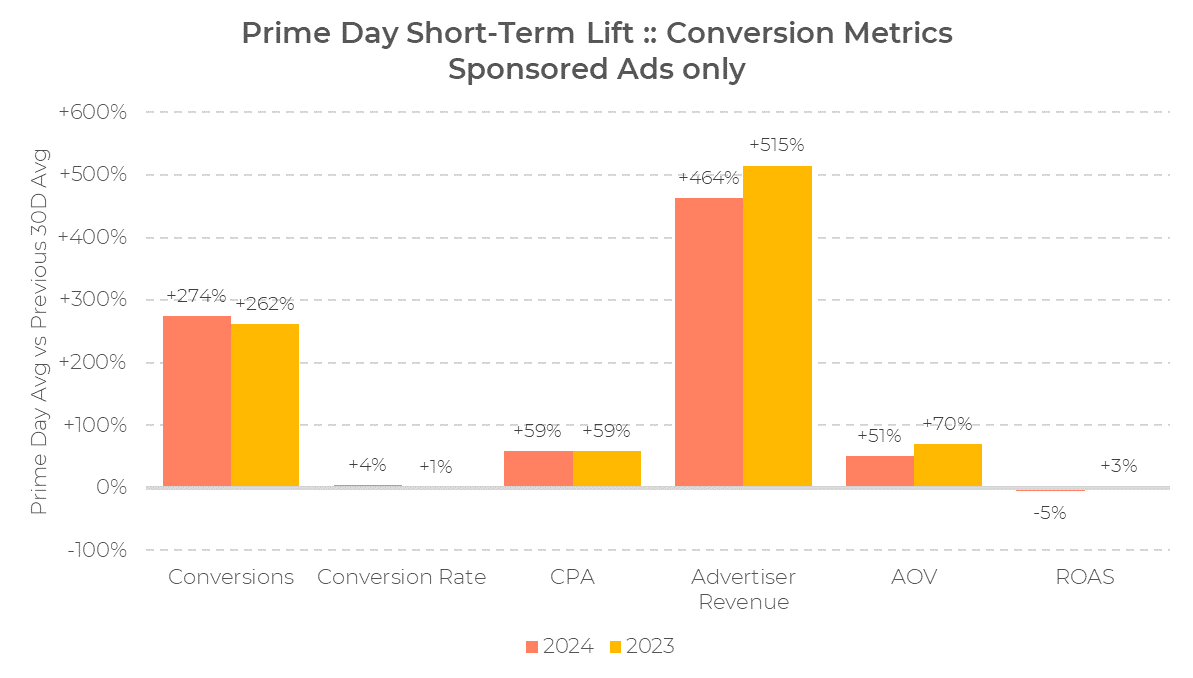

Delivery metrics are only half the picture. What was the short-term lift for conversion metrics? These are conversions and advertiser sales (which can also be described as conversion value), and then all the derived metrics from those two, along with our delivery metrics.

Here, we see some interesting differences between Sponsored ads and DSP in that the display network experiences higher conversion and revenue lift. This is also reflected when we compare Sponsored ads’ short-term lift against the same numbers from last year.

Conversions showed a similar lift to last year, but both Average Order Value and Advertiser Revenue grew less over the prior 30 days this year. So what’s happening?

The year-over-year trends in Prime Day ad spend

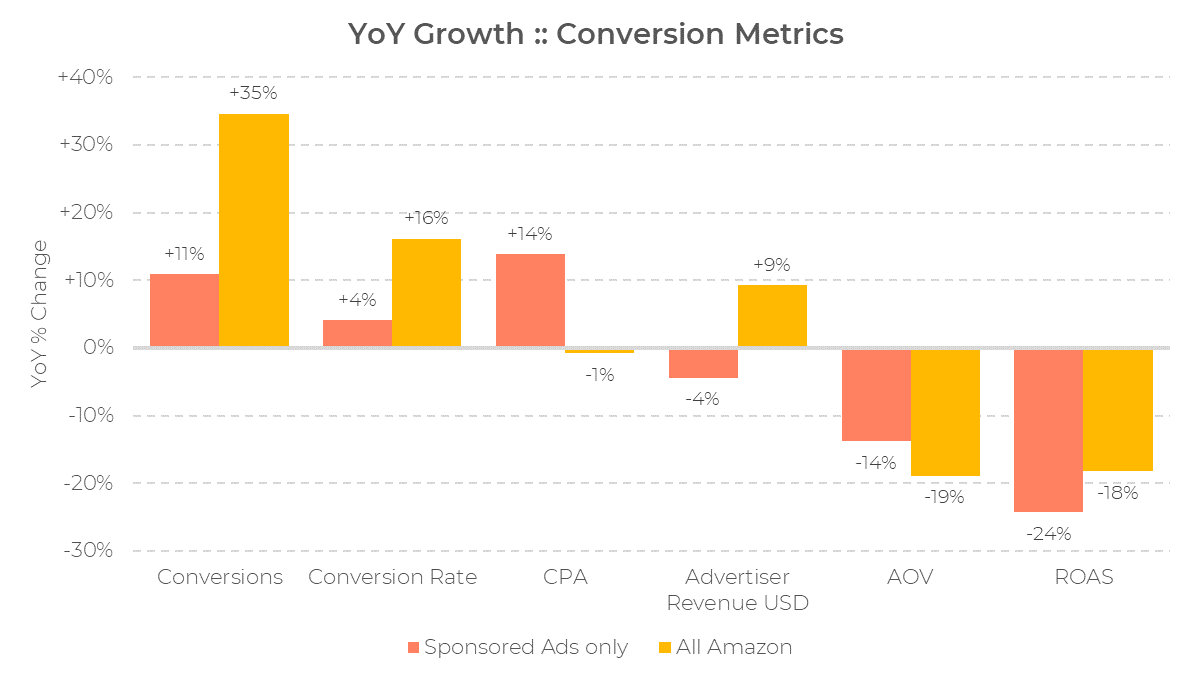

When we look at Sponsored ads on a year-over-year basis, using only Skai accounts that were spent on those Sponsored ads in both years, Advertiser Revenue actually shrinks by 4%. On its face, this is somewhat surprising, but in the context of the short-term lift relative to both DSP and last year, a story starts to take shape.

The best approach seems to be to look at accounts with Sponsored ads spending in both 2023 and then look at the combined spending across Sponsored ads and DSP for those accounts. This keeps the analysis a bit more honest because it allows for incremental DSP spending from existing Sponsored ads advertisers, and this perhaps more accurately reflects the dynamic in the marketplace. We will start with our conversion metrics to show the difference between Sponsored ads on their own, and the combined force of Sponsored ads and DSP.

Why is there such a big difference between Sponsored Ad performance and the combined performance of Sponsored Ads and DSP from the same cohort of accounts?

Clearly, there is some divvying of credit across the two complementary placements that boosts total conversions enough to push advertiser sales revenue higher, even with a lower Average Order Value across the combined total.

When we look at our delivery metrics, the YoY numbers make more intuitive sense. Spending is additive. Conversions and conversion revenue, on the other hand, are zero-sum, so if a shopper clicks on a Sponsored ad and is then retargeted with a DSP ad, or vice versa, the credit for that sale will be split between them in some way based on whatever attribution model is in effect.

All told, we can confidently say that Prime Day 2024 was bigger than Prime Day 2023. Using the right comparison is critical. The interaction between Sponsored Ads and DSP reflects the increasing complexity across retail media.

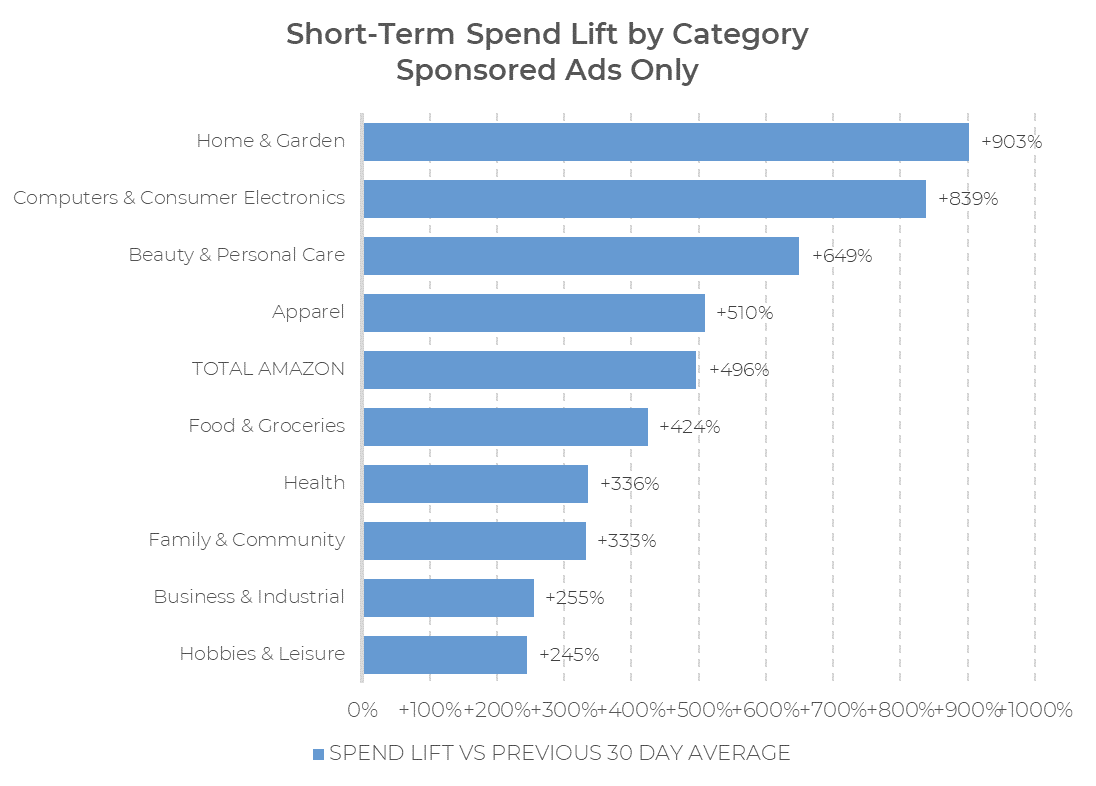

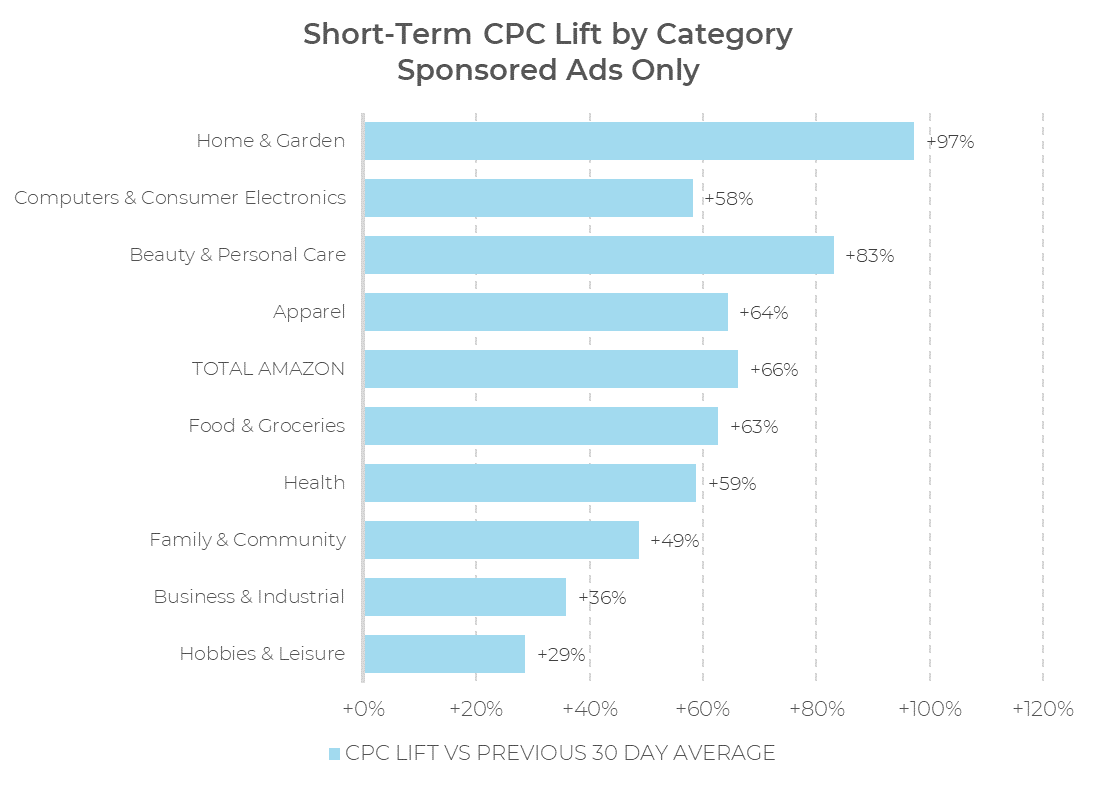

Spending lift by category – a new leader blooms

When we look at differences by category, there’s a new champion when it comes to short-term spending lift: Home and Garden spending grew 10x over the average for the prior 30 days (+903%), possibly riding a wave of seasonality into the warmer months. This edged out Computers & Consumer Electronics, which had typically seen some of the biggest movement in previous Prime Days.

One reason for the surge in Home & Garden was that CPCs nearly doubled in that category, whereas Computers & Consumer Electronics only grew by 58%. After that, most of our categories shake out into nearly the same order as spending lift.

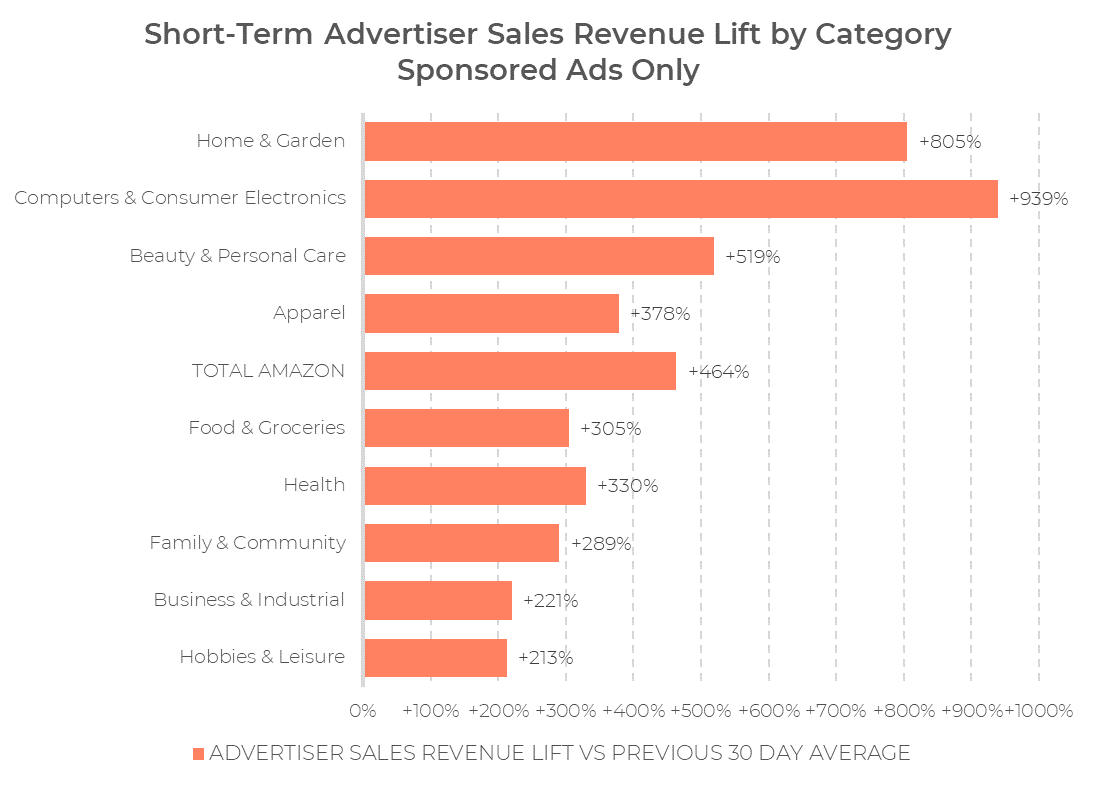

While the Computers & Consumer Electronics category may not have been No. 1 in terms of spending lift, these are typically more expensive items, so it comes as no surprise that when we consider Advertiser Sales Revenue, the category jumps back into the lead, with advertiser sales revenue over ten times the average for the previous 30 days. This is without the additional bump from DSP that we described earlier.

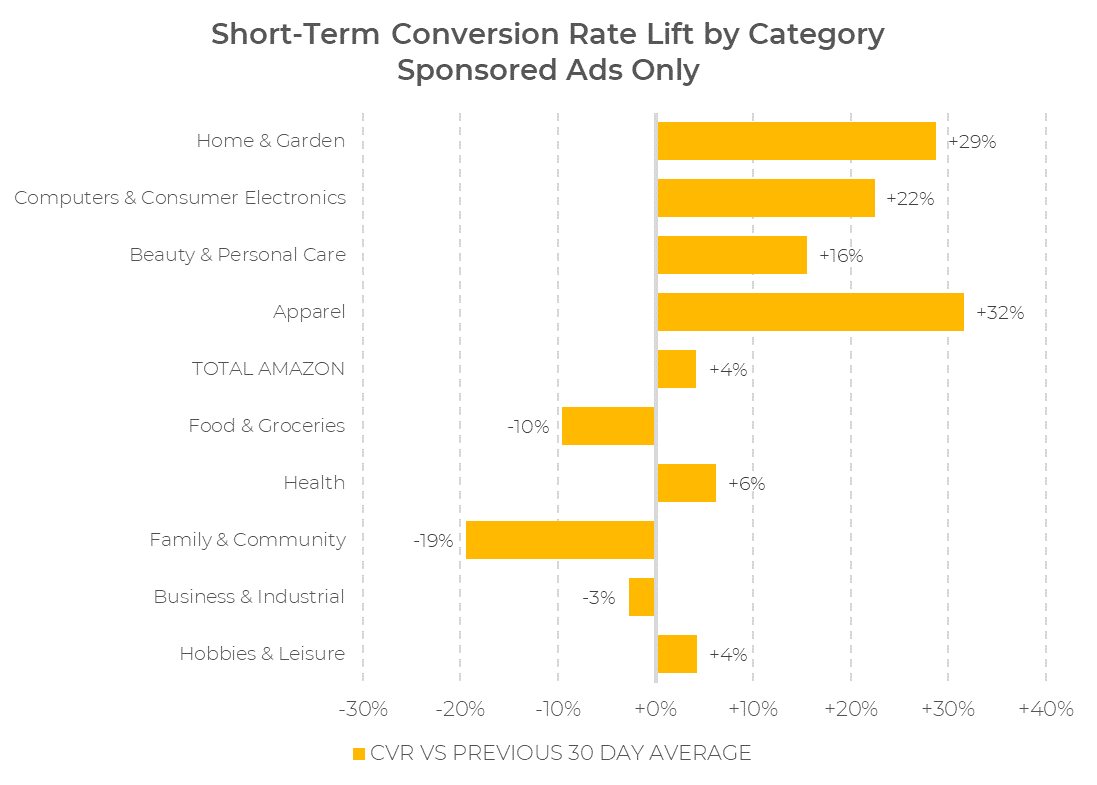

Finally, looking at conversion rate gives us a bit more variation across categories. The three categories that saw lower conversion rates across Prime Day make some sense, as they’re all more closely associated with everyday items (groceries, baby & parenting, and office supplies) and not the “splurge” items that are heavily marketed for the event.

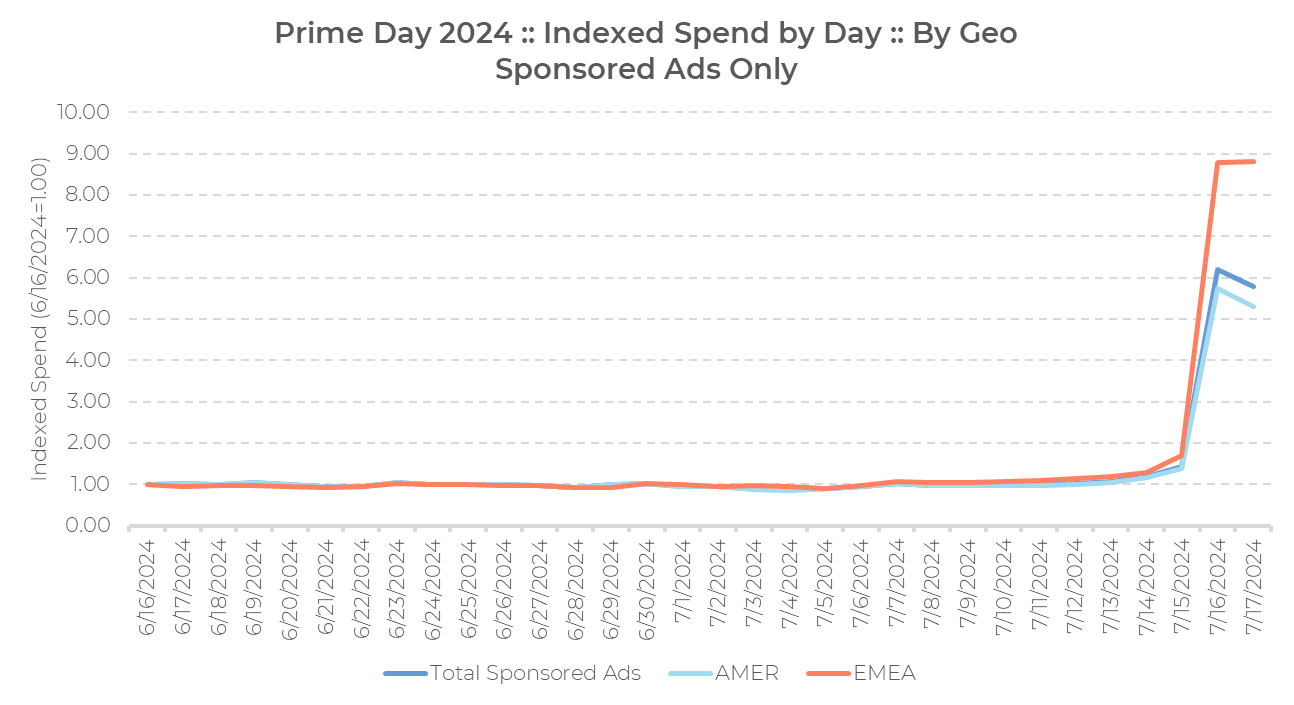

Prime Day lift by geographic region

When we separate out our two largest geographical regions, we can see that EMEA saw a bigger spike on Prime Day. Note that each line is indexed separately, independent of relative size — this does not imply that AMER and EMEA spend was identical on June 16.

The following table shows how key lift metrics differed across these two regions. Spend, CPC, and Advertiser Sales Revenue all showed bigger increases in EMEA, while AMER saw a bigger change in Conversion Rate. It is likely that Prime Day is both larger and a bit more mature in the Americas, giving EMEA more room to grow in the short term.

| Total(Sponsored Ads) | AMER | EMEA | |

| Spend | +496% | +453% | +753% |

| CPC | +66% | +64% | +97% |

| Advertiser Sales Revenue | +468% | +407% | +713% |

| Conversion Rate | +6% | +7% | -0% |

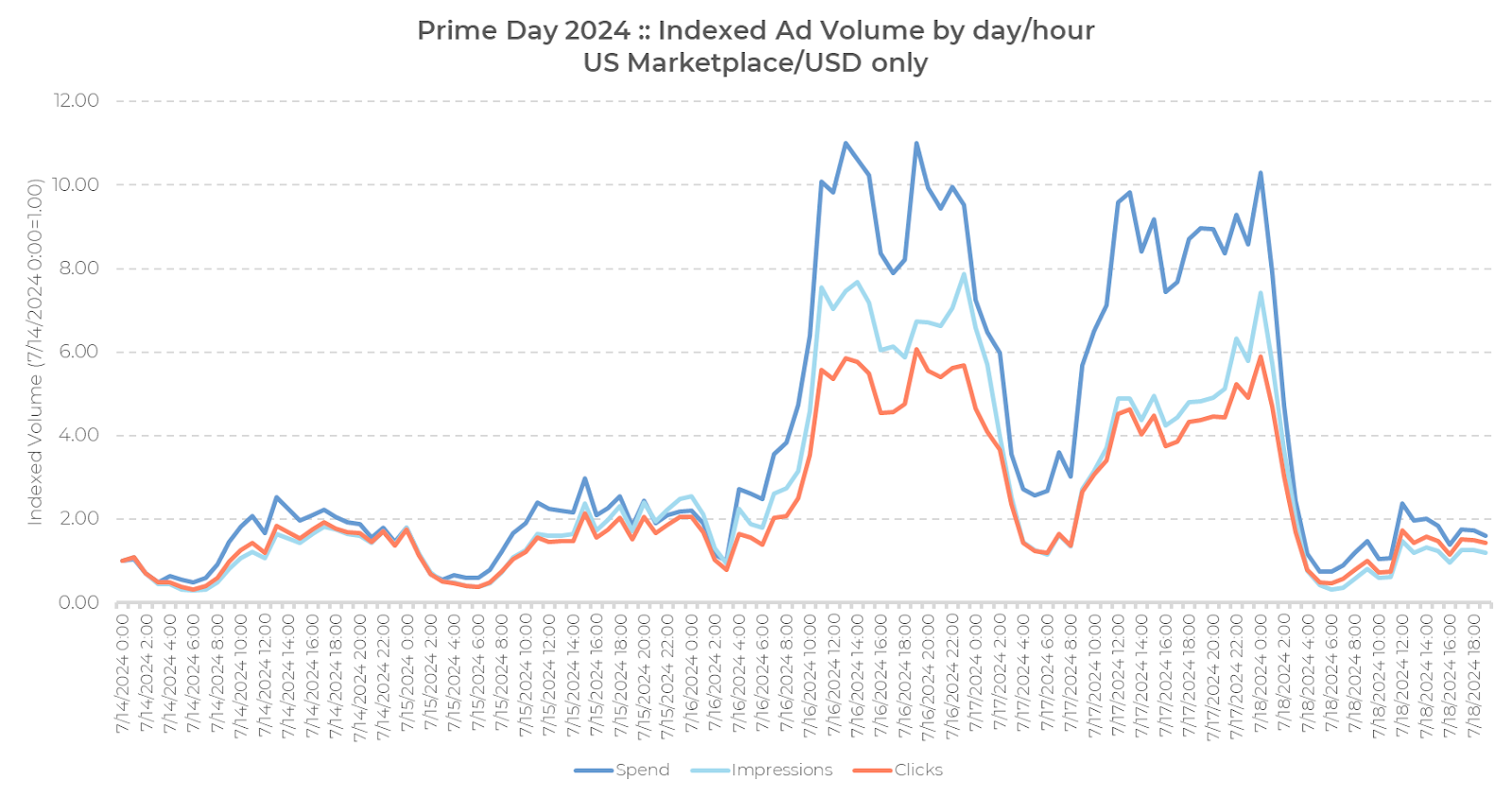

Prime Day hour-by-hour

Next, we can examine US Amazon data for peaks across the two-day stretch. For this analysis, we fix the left-most point at 1.00 and index every subsequent hour relative to that. All times are Eastern Daylight Time.

Here, we will only consider delivery metrics, and we can see that:

- On Tuesday (day one) spending peaked at 1 pm EDT and then again 5 pm EDT, with two high-spending periods running from 11 am to 3 pm and 7 pm to 11 pm.

- On Wednesday (day two), volumes were somewhat lower, with an early peak from 12 pm to 1 pm and a late peak towards the end of the event at midnight Eastern time (9 pm PDT). Spending was elevated from 11 am straight through to midnight EDT, with the exception of a slight lull in the late afternoon between 4 pm and 5 pm.

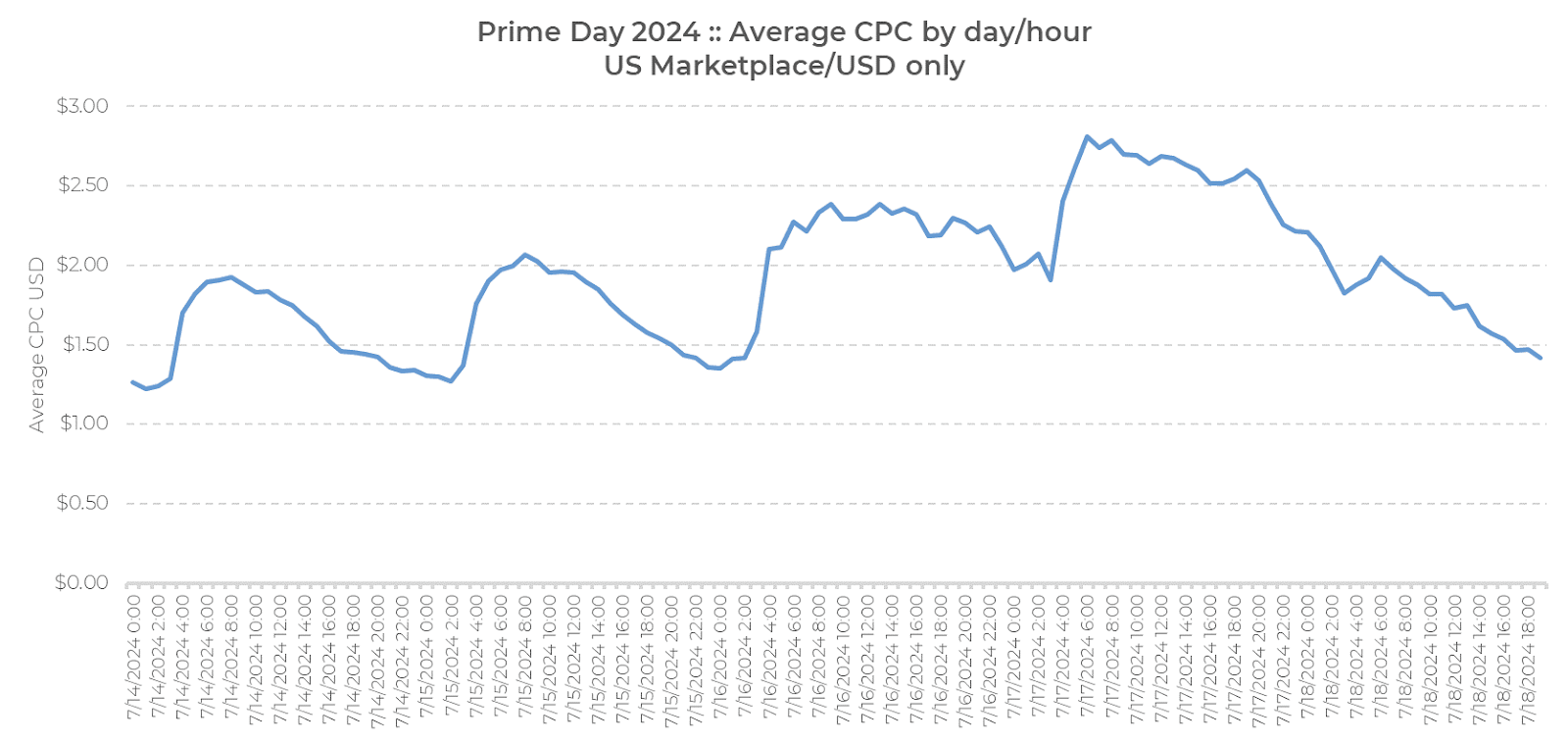

For ad prices, CPC peaked at 1 pm EDT on day one at $2.39 and then at 6 am on day two at $2.81, kicking off a stretch of prices ~20% higher than on Tuesday. This is for Sponsored ads only.

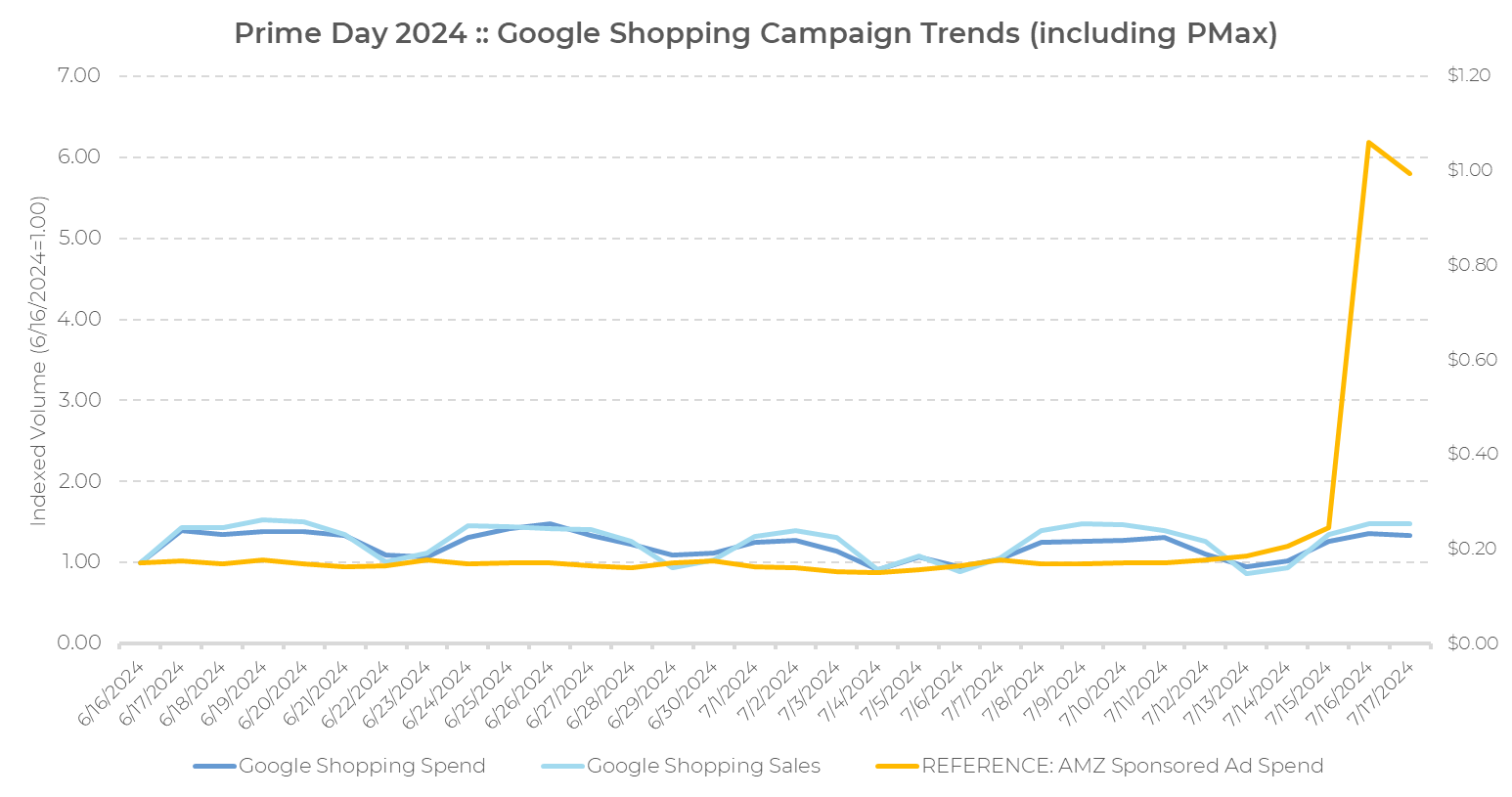

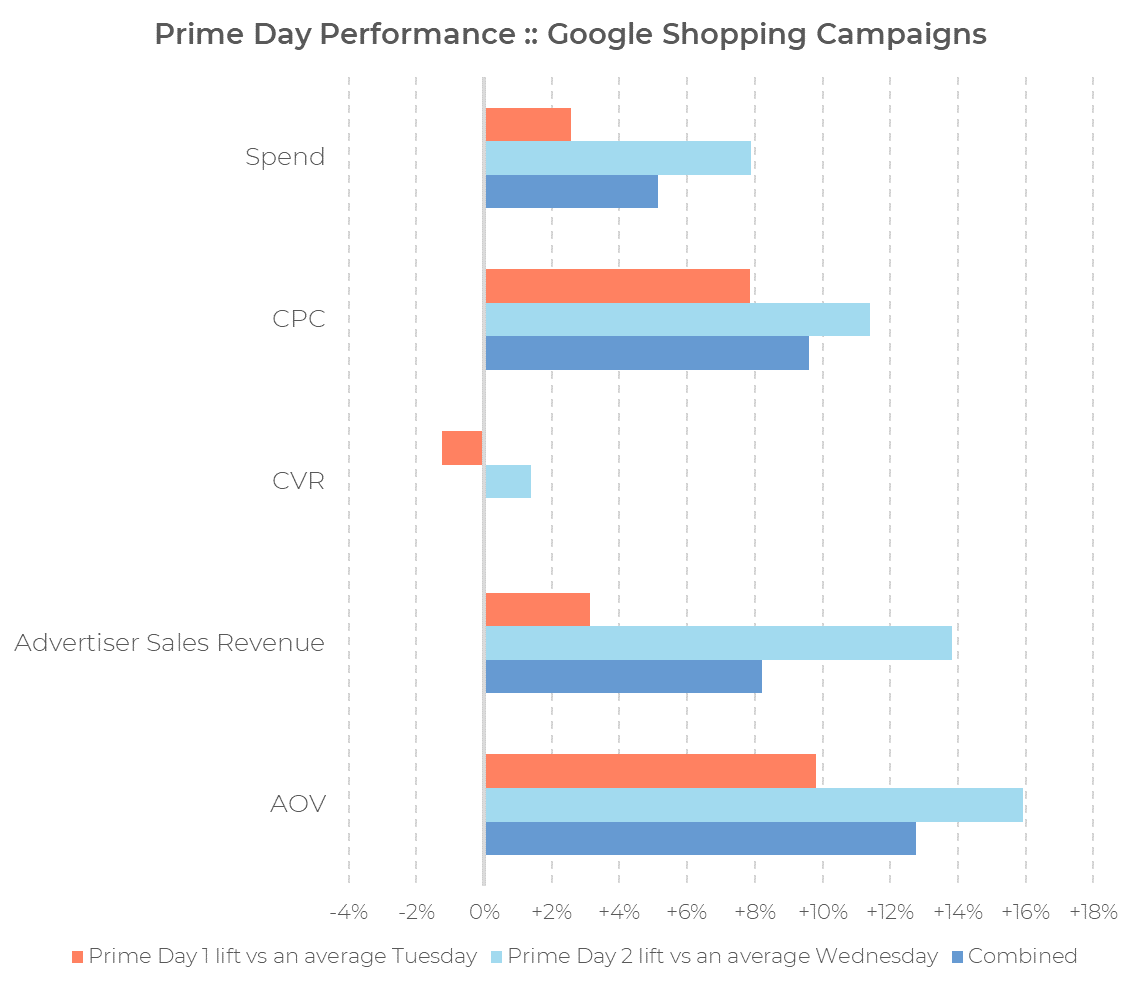

A proven Prime Day halo effect?

In the past, there has not been any particularly compelling evidence that Prime Day spills over into other digital marketing channels, but this year, that has changed. Some of this may be due to fine-tuning our analysis to recognize some of those channels’ unique qualities and measure them accordingly.

For example, search shopping campaigns on Google, including the newer Performance Max campaigns. If we simply look at daily trends over our 32-period, any consistent lift similar to what we see with Amazon spend is dwarfed by the normal periodicity of shopping campaign trends over the course of the week.

To control for this, rather than looking at the daily average across all 30 days, we can look at the average for the four Tuesdays and four Wednesdays in the 30-day runup, compare Prime Day’s Tuesday and Wednesday to an “average” Tuesday and Wednesday, and then look at both days combined.

What we see is that CPCs are higher, driving up spending, but that a double-digit increase in Average Order Value pushes Sales Revenue higher enough to offset that additional budget. While there may be other factors driving these numbers higher, the timing does not appear to be a coincidence.

No end in sight for Prime Day’s success

Prime Day continues to grow. The spike over the prior 30 days continues to get bigger from year to year across nearly all metrics. Its footprint has expanded significantly into DSP to the point where a holistic view of Amazon’s performance is necessary to see the full growth picture. Big-ticket categories like Home & Garden and Computers & Consumer Electronics continue to be big winners for the event, while everyday items are less of a focus. And there does seem to be a spillover in performance for paid search.

All of these have been fairly durable findings over the years that Prime Day has existed, so be sure to bookmark this post for future reference to be fully prepared next time. That goes for Amazon’s anticipated companion event in October as well, albeit to a lesser degree. Looking ahead to Cyber 5 (the five-day shopping period from Thanksgiving to Cyber Monday) and into December, we expect Prime Day ad spending to again outpace Q4 holiday advertising.

Skai helps you maximize Amazon on Prime Day – and every day

Skai’s Retail Media solution empowers marketers to plan, execute, and measure digital campaigns that meet consumers when and where they shop. As part of our omnichannel platform, we connect the walled gardens and manage campaigns on 100+ retailers, including Amazon, Walmart, Target, and Instacart, alongside major publishers across paid search, paid social, and apps.

For more information, schedule a brief demo to see how our Amazon Ads support can help boost your full funnel strategy every day of the year.

More like this

-

Monthly Industry Snapshot – October 2024

-

Monthly Industry Snapshot – September 2024

-

Monthly Industry Snapshot – August 2024

-

Monthly Industry Snapshot – July 2024

-

Roundel Media Studio: Democratizing Retail Media for Small and Medium Businesses

-

Key Takeaways from the Skai Q2 2024 Quarterly Trends Report