Summary

Amazon Prime Big Deal Days 2024 continues to grow as a significant sales event, showing a 250% increase in ad spending compared to the previous 30 days. Advertiser revenue increased by 258%, with the Home & Garden and Computers & Consumer Electronics categories being standout performers, with spending lifts of over 400%. While Big Deal Days has yet to match the scale of Prime Day or Black Friday, it remains a growing event with its own unique value.

Over the last three years, Amazon’s fall sales event has established a consistent pattern as a sort of younger sibling to the more established Amazon Prime Day in early summer as well as the unofficial start to the holiday shopping season. Originally called the Prime Early Access Sale, this October event has been known as Amazon Prime Big Deal Days since last year, and we have analyzed advertiser performance around the 2024 edition to better understand just how big of a deal it is.

Methodology: The following analysis is based on Amazon ad spending hosted on the Skai platform across both Amazon Sponsored Ads and Amazon DSP. For comparative analysis across time periods, only named Skai accounts with spending across both periods in the comparison are included. All other analysis includes all accounts.

Prime Big Deal Days 2024 insights

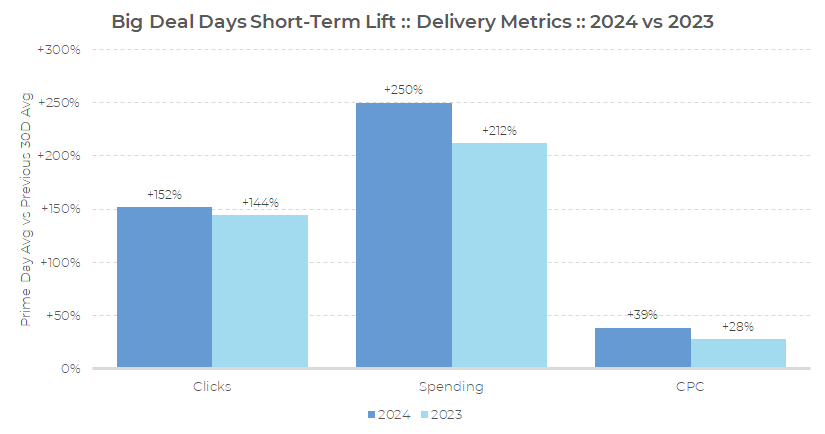

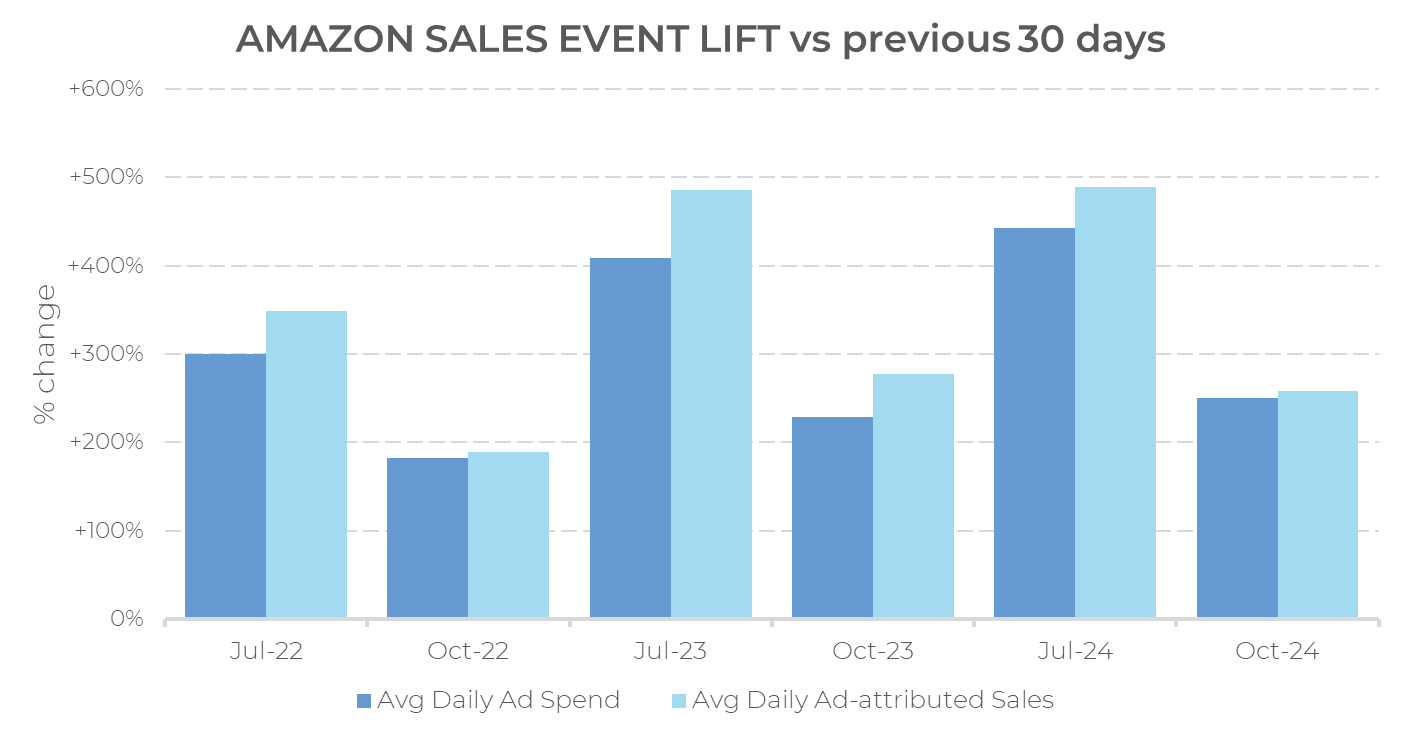

The first way we look at performance for big sales events is by looking at the event days versus the average for the previous 30 days. Through that lens, average daily spending grew +250%, or 3.5x. This was slightly higher than last October, which posted a spending lift of +212%.

This was the result of increases to click volume (+152%) and average cost-per-click (+35%), which both saw greater lift than the same event last year.

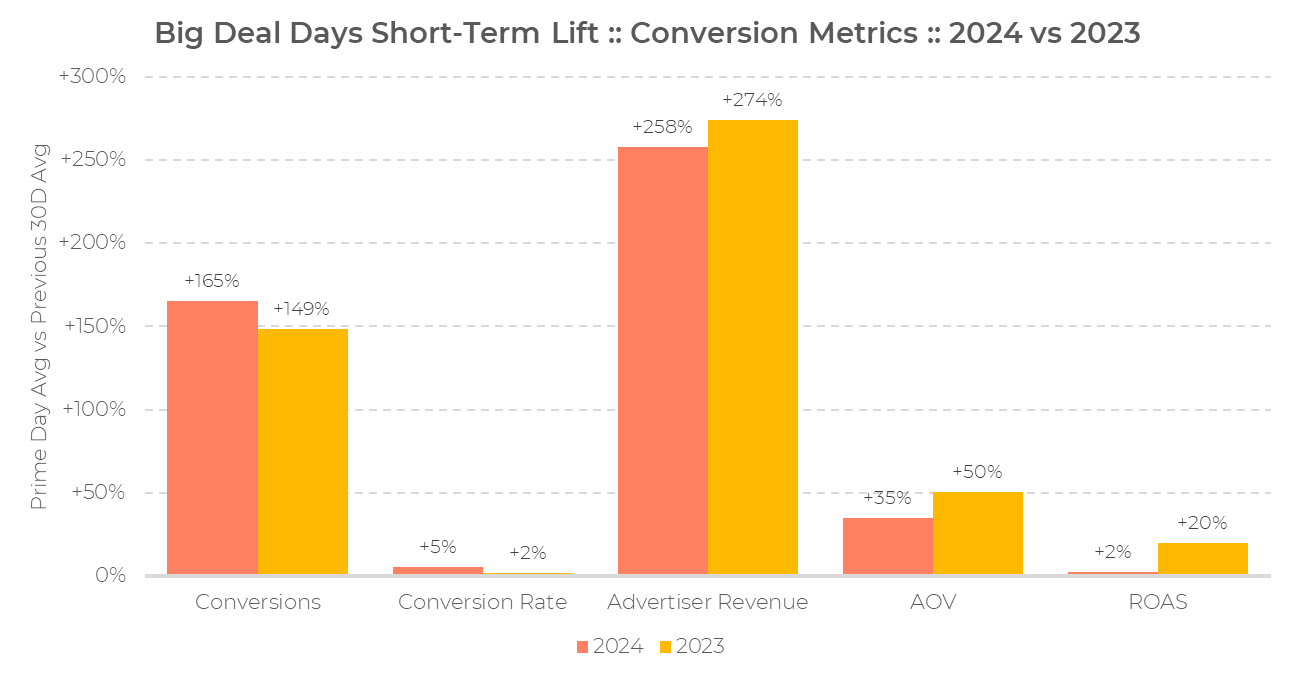

Getting ads in-market is one thing. Generating sales is another. From that perspective, Big Deal Days saw a +165% increase in conversions and +258% increase in ad-attributed advertiser revenue, or conversion value. That lift in advertiser revenue was ~20 points less than last year, which is attributable to last year having a larger average order value (AOV). This, in turn, may come down to a different mix of categories and products that emphasize different price points.

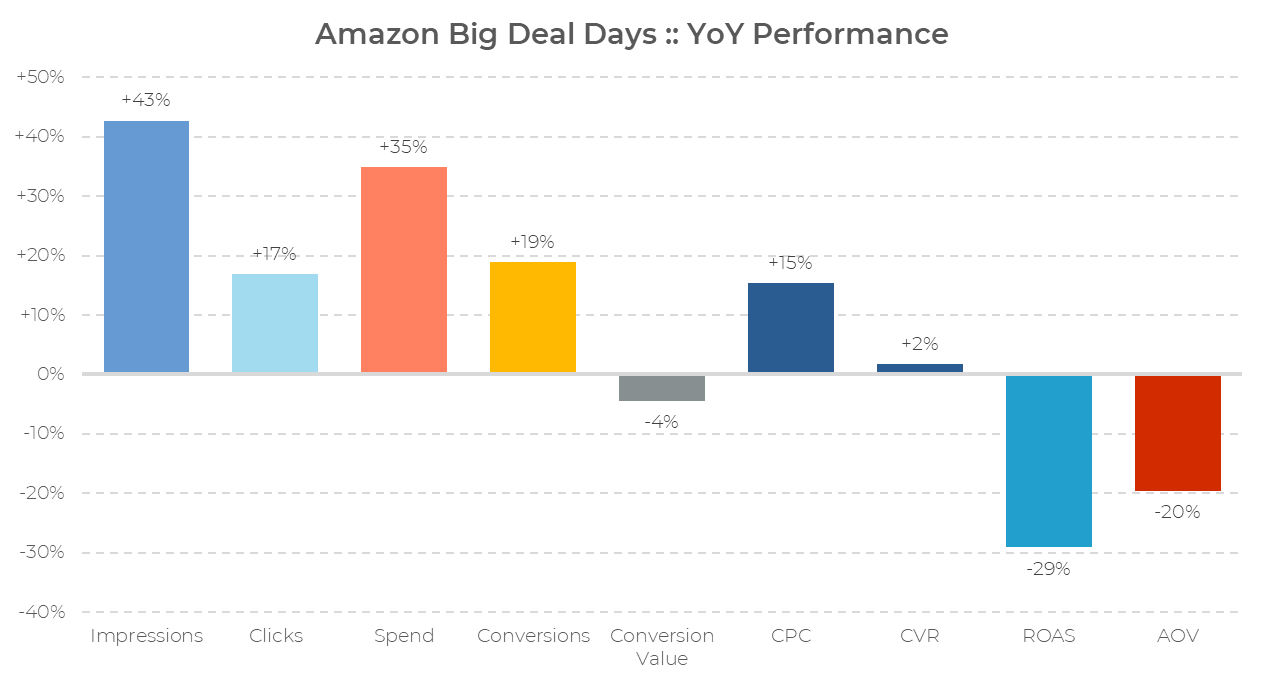

Looking at the lift generated by Big Deal Days versus the previous 30 days for this year and last year is one way to compare performance over time. Another way is to directly measure metrics for the subset of Skai accounts that were active in both years. Here, as well, we can see how the lower average order value brought total advertiser revenue and ROAS down from last year’s event.

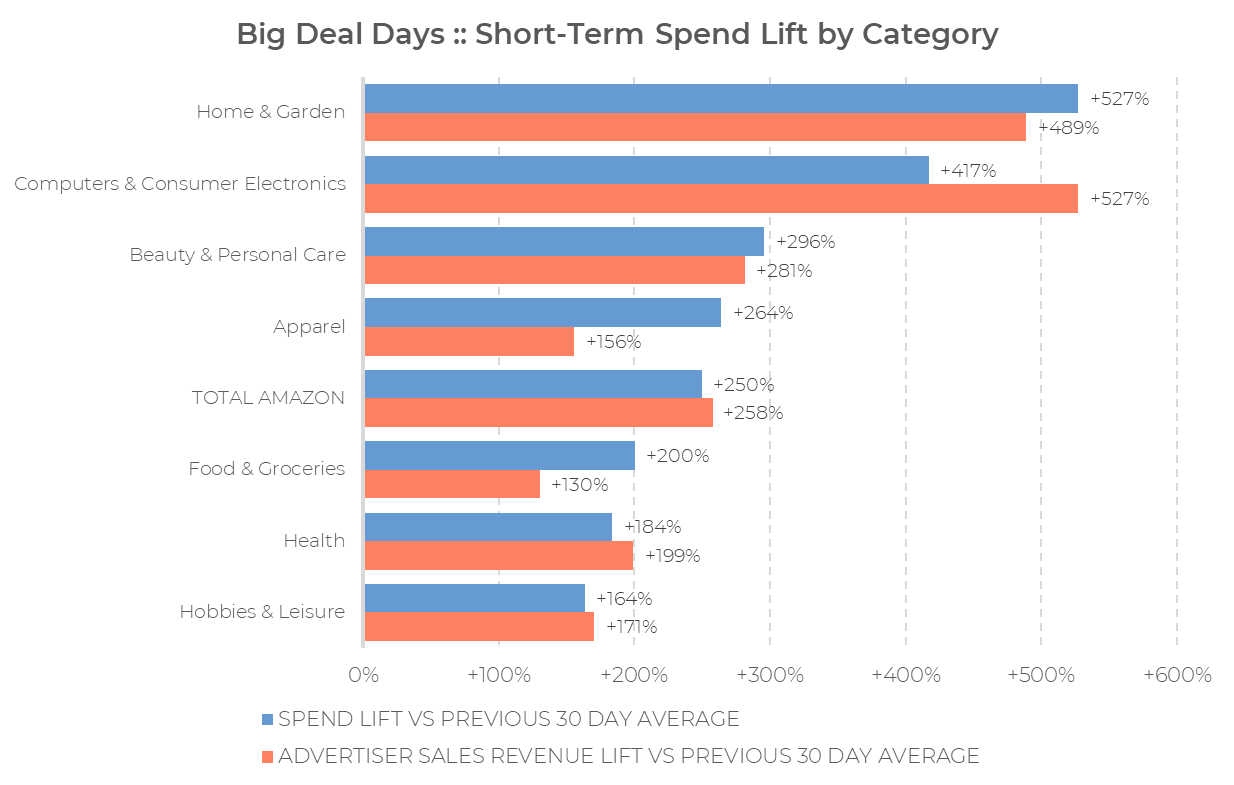

When we break down Amazon’s performance by category, Home & Garden and Computers & Consumer Electronics are the clear standouts, with spending increasing by +527% and +417%, respectively. In both cases, advertiser sales revenue mostly kept pace, with the tech category seeing a bigger spike in sales that point to an increase in ROAS for the event. A big deal, indeed.

Finally, we have to consider how Big Deal Days stacks up against the summer Prime Day event. The answer is fairly consistent in that the impact on both spending and sales revenue is about half that of the July Prime Day, and both have seen increases in spending over the last three years. Sales revenue lift was mostly unchanged over the last two years for Prime Day and slightly down for Big Deal Days, as shown previously in this analysis. Again, this may be due to a shift in product mix over time, but it also could point to an unusually strong macroeconomic environment last year, in that economic news repeatedly outperformed expectations.

So, on the one hand, the Big Deal Days event has a definite impact on aggregate advertiser and shopper behavior, and that impact is growing over time for most metrics. On the other hand, sandwiched between Prime Day and Black Friday, it is unlikely to close the gap in the performance of those two events in the near future, but one can argue that Big Deal Days is not in competition with those other events, and is, in fact, a big deal on its own merits.

More like this

-

The 2026 State of Amazon Ads: What’s Working, How Advertisers Are Leveling Up, and What the Industry Can Learn

-

The 2026 State of Retail Media Fragmentation: 7 Challenges Brands Must Solve to Scale

-

The 2026 State of Retail Media DSP, CTV, and Social Commerce: Accelerating Beyond the Shelf

-

2026 CPG Industry Preview: Food & Beverage Marketing Guide

-

AI, Automation, Authenticity: The Three Trends Redefining Social Commerce

-

The 2026 State of Retail Media Measurement and Incrementality