Spending and Pricing Trends Across Paid Search, Social Advertising, and Retail Media

Spending across key digital marketing channels varied greatly in July. Retail media got a big boost from Amazon Prime Day that drove a 24% increase in spending, while paid search saw a number of large advertisers tap the brakes to start H2, with spending down 8% even in a slightly longer month. Paid social spending did not change.

Prime Day also provided a tailwind for higher retail media CPC, up 12% over June. Paid search click prices and paid social CPM both dropped, by 1% and 6% respectively, which should come as a relief to digital marketers increasingly concerned by ad price inflation.

How do you measure up? Check out these benchmarks to see if your programs are on par with your industry peers, ahead of the curve, or behind the curve.

This is a continuation of our monthly paid media snapshot series. As with any benchmark, your mileage may vary, but we hope this provides a bit more context for you as a marketer as you navigate the ups and downs of your program’s performance.

Monthly Industry Snapshot – July 2024

Methodology: Only Skai accounts with spend above a minimum threshold for the previous three months are included in these benchmarks. Please note that the selection criteria used here differ from the Skai Quarterly Trends Report and may not be consistent with those results in all cases. Starting in November 2023, paid social data has been expanded to include Meta, Pinterest, TikTok, LinkedIn, and YouTube.

How to read these charts

Accounts are divided into segments based on increases or decreases of at least 5% in monthly spending and CPC for retail media and paid search or CPM for paid social. Those segments are then plotted on a bubble chart where the x-axis represents the month-over-month (MoM) percent change in pricing for that segment, and the y-axis is the MoM percent change in total spending. Bubble size represents the percent of total Skai accounts.

The diagonal line indicates spending changes that are completely described by the change in pricing. Bubbles above the diagonal mean that ad volume—clicks for retail media and paid search, impressions for paid social—grew faster than pricing. In contrast, bubbles below the diagonal mean that volume grew slower.

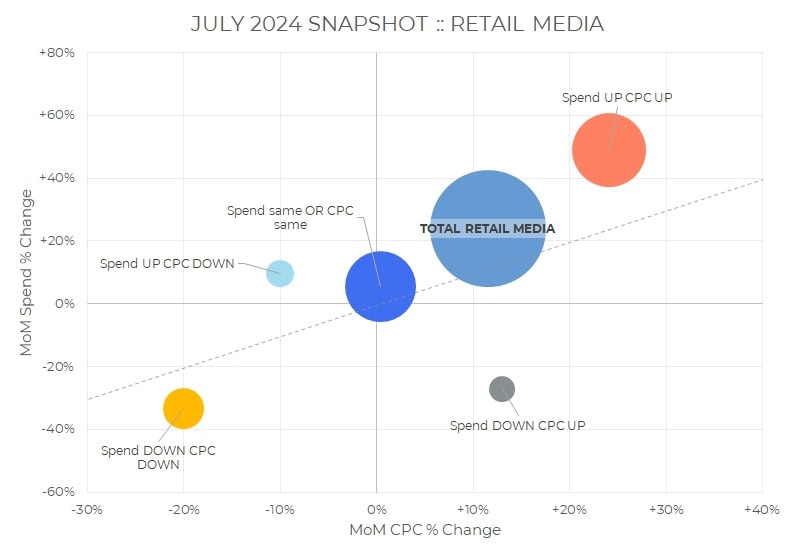

Retail Media

Overall, retail media spending grew 24% in July, while average CPC increased 12%. Average spending per day rose 17%.

- 63% of retail media accounts spent more in July than June compared to 23% who spent less, and the average price of a click increased for 48% of accounts and decreased for 21%, with the remaining share for each metric seeing no change.

- Of the segments that showed movement in both spending and pricing, the largest was where both spend and CPC increased, which comprised 40% of all retail media accounts in the analysis. Another 37% showed no change in either spending levels OR the price per click

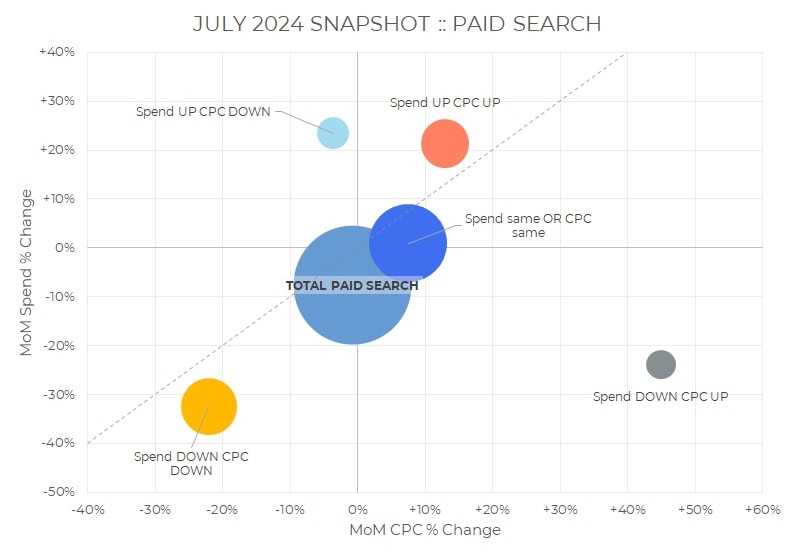

Paid Search

Overall paid search spending decreased 8% in July, while average CPC dropped 1%. Average spending per day dipped 11%.

- 39% of search accounts spent more in July than June compared to 37% who spent less, and the average price of a click increased for 31% of accounts and decreased for 37%, with the remaining share for each metric seeing no change.

- Of the segments that showed movement in both spending and pricing, the largest was where both spend and CPC decreased, which comprised 24% of all paid search accounts in the analysis. Another 45% showed no change in either spending levels OR the price per click.

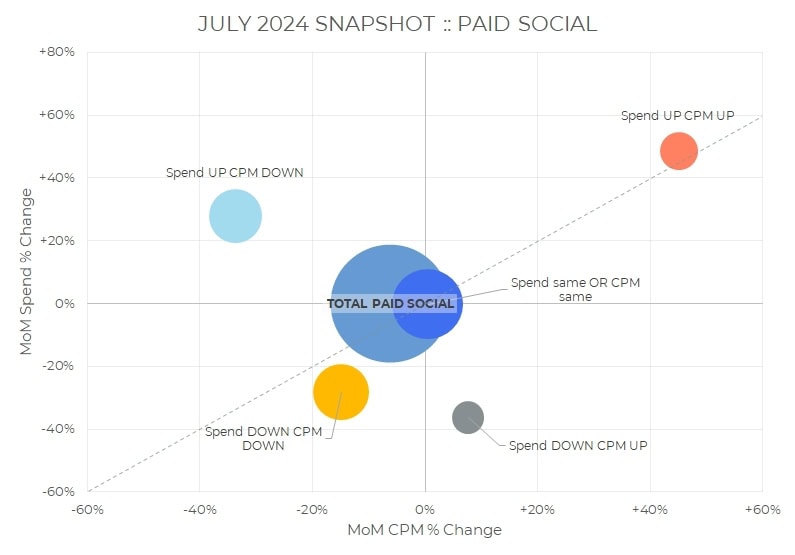

Social Advertising

Overall, paid social spending stayed level in July, while average CPM decreased 6%. Average spending per day dipped 3%.

- 44% of social accounts spent more in July than June compared to 39% who spent less, and the average price of one thousand impressions increased for 21% of accounts and decreased for 54%, with the remaining share for each metric seeing no change.

- Of the segments that showed movement in both spending and pricing, the largest was where both spend and CPM decreased, which comprised 23% of all paid social accounts in the analysis. Another 37% showed no change in either spending levels OR the price per thousand impressions.

Check out more resources from Skai

Come back next month for the most up-to-date data. Until then, you can dive into more of our research via our Quarterly Trends Reports hub.

Please visit The Breakthrough and the Skai Research Center for ongoing insights, analysis, and interviews on all things related to digital advertising.